Studying Winning Stocks: Amazon in 2012

The Best Stock Pitch I've Ever Seen

One of the best ways to become a better investor is to study winning stocks. In fact, I believe that rather than figuring out what to avoid when making an investment, a far better ROI can be had by learning what makes a winning stock instead.

As a result, I enjoy analyzing past wonderful investments. Here are two that I’ve shared before:

Nicholas Sleep’s Costco from June 2005 (+20x since 2005, without dividends)

Norbert Lou’s NVR from June 2001. (+30x since 2001)

What’s amazing about the stock market is that you didn’t even need to come up with these wonderful ideas. But, if the investment thesis made sense to you, and if you could build your own conviction, you could have made 20-30 times your money!

Today, I want to talk about the best stock pitch I’ve ever seen:

Josh Taroff’s (Greenlea Lane Capital) AMZN stock pitch from VALUEx Vail 2012 [Like to Pitch Deck]

The Stock Recommendation

Recommendation: Buy AMZN @ $218.35/share (~$100 Billion market cap at the time)

When: June 15 2012

What Happened Next?

AMZN has obviously turned out to be a massive winner:

Doubled in a year

Tripled in 3 years

4X’d in 4 years

6X’d in 5 years

10X’d in 7 years

19X’d in 9 years

Unbelievable.

Simply unbelievable.

How could we have evaluated the investment opportunity in 2012?

Of course hindsight is 20-20 but could we have developed the conviction to buy the stock had we come across the investment writeup in 2012?

To answer this question, one framework I like to use is to answer the following:

Do I understand the Business?

Does the business have a durable competitive advantage?

Is the company management talented and can they be trusted?

Can I buy the business for a reasonable Price?

Let’s start.

First, Josh says that the company is trading at a whopping 179x trailing GAAP EPS but he also claims it’s very cheap.

That’s interesting. In fact, that’s very interesting, because conventional wisdom says that 179x is ridiculously expensive.

Why does he think that?

Let’s find out.

Question 1: Do I Understand the Business?

At the time of the pitch, Amazon was worth $100 Billion, and it was quite well known. In fact, we were all likely Amazon customers. So understanding the business should not have been too hard.

Here’s how Josh described it:

For those of you who read my analysis of the Costco investment pitch, this should sound familiar, it is exactly what Nick Sleep referred to as “Scale Efficiency Shared with Customers”.

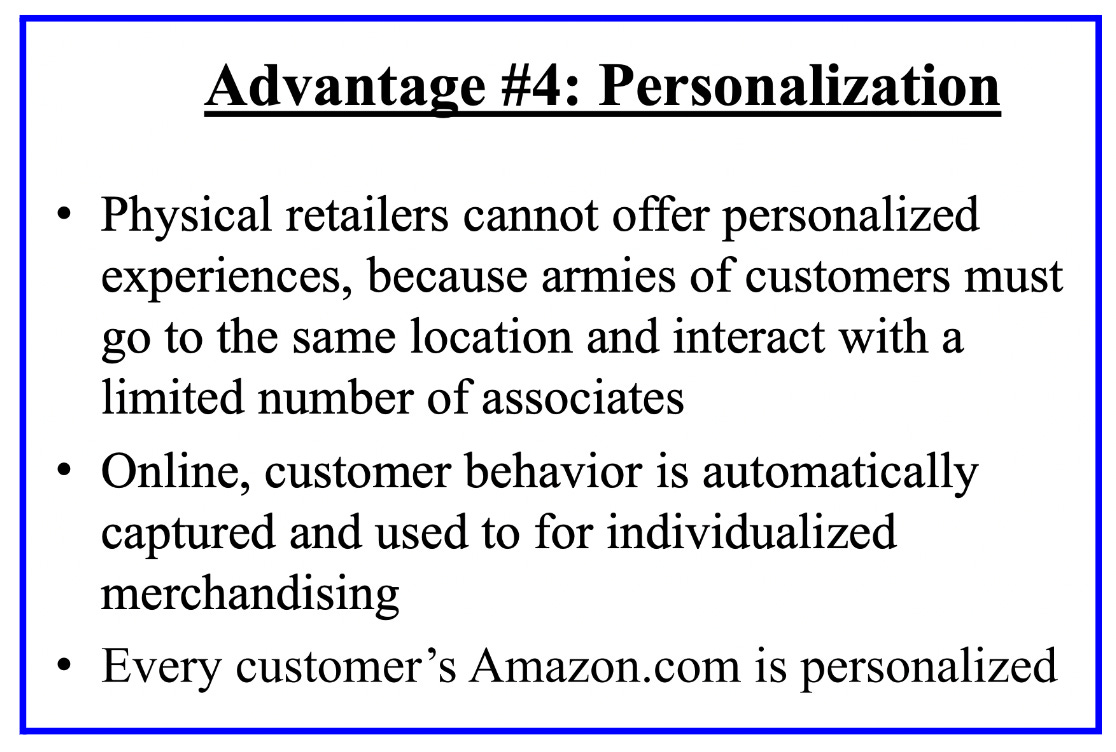

Question 2: Does the business have a durable competitive advantage?

Josh outlines Amazon’s competitive advantages, and does so in very simple, easy to understand terms.

One of the hardest parts about investing is understanding a company’s sources of competitive advantage. Peter Thiel refers to these as “secrets”.

“Great companies have secrets: specific reasons for success that other people don't see.”

— Peter Thiel.

A secret however can be devilishly hard to uncover. One reason: Secrets often don’t seem like much, even once they are out in the open.

Take the advantages listed above. They are quite intuitive. But they don’t seem like much, especially advantages 2-5. That makes them easy to dismiss.

For example, for me, Advantage 5: Habit Formation, would likely have been easy to dismiss in 2012. I suppose I would have attributed an advantage to the Amazon brand, not necessarily habit formation. Perhaps there is overlap? In any case, I’m not much of a shopper, but I can now see how buying on Amazon repetitively could build such a habit. After getting married, I certainly see this more clearly now. My wife is always ordering one thing or another from Amazon…it feels like there’s always a package at my front door, just waiting for me to bring inside.

Another thing that stood out to me was Josh’s claim that “Amazon’s availability is analogous to Coke’s ubiquity”. This was quite a profound insight. And frankly, it's very hard to internalize, even today.

Lastly, and importantly, Josh states that all these advantages are widening.

If you agreed with the above, it was clear that Amazon possessed a durable competitive advantage. In fact, one that was growing.

The company was already a mega cap by then, and as such, agreeing with this conclusion was likely not difficult. Especially, since Josh’s pitch expected the business to be largely the same in the future, just bigger and stronger.

Question 3: Is the company management talented and can they be trusted?

Josh doesn’t talk much about this in his stock pitch. That said, Jeff Bezos had already become a pretty household name by 2012. He was very well regarded and respected for what he had accomplished.

One could have read his shareholder letters to get a window into how he thought about Amazon, and business in general.

Plus, considering the company had been led by the same person from the getgo to the point that it was now worth $100 Billion, I don’t think it was a large leap to agree that management was talented and could be trusted.

That said, determining management quality is a very subjective and personal skill. You’d have to come to a conclusion yourself.

Next, Josh talks more about Amazon’s strengths, specifically the company’s :

Long term focus, and

Dominant market position in both physical and online retail

Question 4: Can I buy the business for a reasonable Price?

At this point Josh moves onto what is likely the most controversial component of his stock pitch: valuation.

If someone is willing to pay 179x trailing GAAP EPS, they better feel confident about sustainable future growth.

Josh claims that growth is accelerating because of Amazon’s Third Party Marketplace (3P) business.

He makes an astute observation that unit growth is a better indicator of earnings power, instead of revenue growth. This is because marketplace fees, as opposed to gross sale values, are booked as revenue (and a result are only a fraction of that in the retail busines). And because operating profit is similar regardless of whether Amazon sells a product themselves or via 3P.

As a result, looking at revenue misses the extent of growth being experienced. Revenue growth was 40% in 2011, but unit growth had accelerated and grew at 49%.

This makes sense.

But then the question becomes, is this growth sustainable long term?

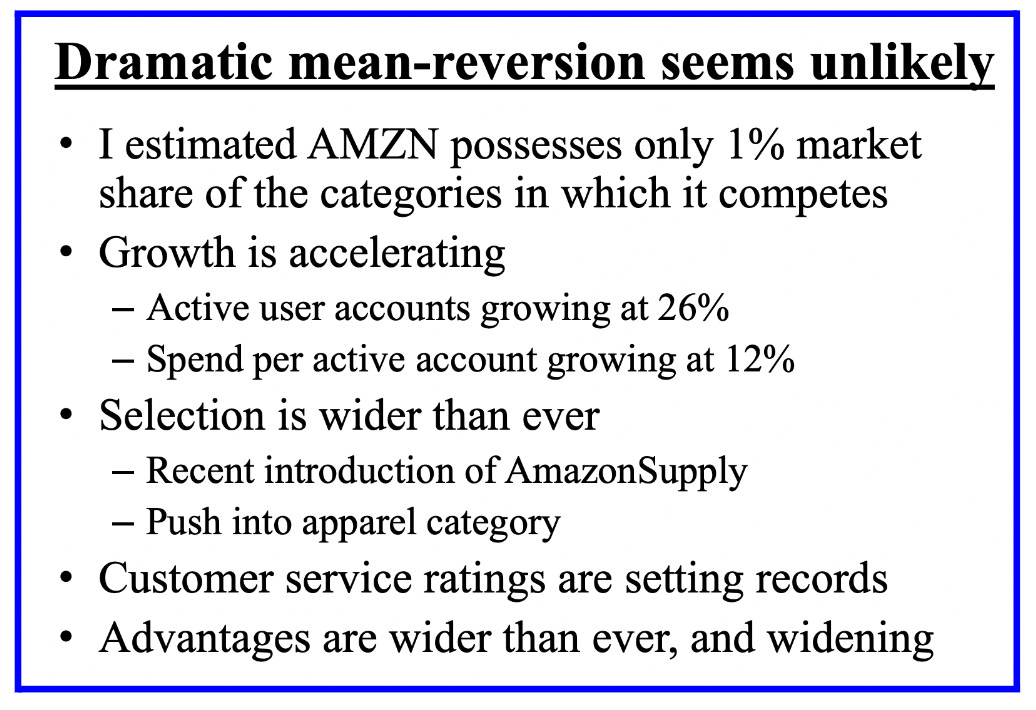

Josh argues that eCommerce is an underestimated significant tailwind for Amazon. Data showed that both eCommerce growth was accelerating, and so was eCommerce as a percent of total retail.

Josh’s qualitative assertions made a lot of sense. Therefore, I bet one of the primary points of friction for most investors who didn’t invest in Amazon at the time was whether revenue growth would decline.

Josh claimed that revenue growth reversion to the mean was unlikely, but frankly, even if it reversed, the prospective 10-year CAGR would still be quite high.

The big leap of faith he made was that eCommerce penetration would reach ~20% in 10 years. And since Amazon was growing at 3X the industry growth rate, Amazon’s growth CAGR would be significantly higher.

To invest, you had to believe this.

I tend to be more qualitative in my analysis, but this example is a wonderful demonstration on how one can marry both the qualitative and the quantitative in a relatively straightforward way.

How Josh married the two was simply amazing. I love the simplicity and elegance of his thought process.

The next hurdle an investor needed to overcome was related to Amazon’s profitability. Conventional wisdom at the time was that Amazon doesn’t make any money.

Josh argued that this was incorrect. Specifically, he said that Amazon was in hyper growth, and as a result, that depressed GAAP margins. Therefore, investors should focus instead on “normalized margins, not GAAP margins”. He defined Normalized Margins as the pretax cash flow that would be available for distribution to shareholders, if Amazon weren’t aggressively investing in growth.

Below is how he how he demonstrated that Amazon was in fact very profitable. For those who are less comfortable with adjusting financial statements, you can learn a lot from the slides below.

Ok, that tells us that Amazon was in fact profitable (if it wanted to be), but it didn’t quite answer the valuation question we laid out above.

We’re getting there...

Josh used EV/NOPAT as his valuation metric.

He calculated the trailing 12 month multiple to be 39x and the forward multiple to be 28x (assuming 7% EBIT margins and a 30% tax rate).

The 7% EBIT margin assumption is quite appropriate. He argued that Amazon’s normalized operating margins should be greater than the 7% EBIT margins of WMT and TGT (much more mature and best in class leaders in retailing), because Amazon had no physical locations, more efficient distribution systems, little shrinkage, and that the 3P business had much higher margins than traditional retail.

He then calculated Amazon’s adjusted ROIC. Notice how it’s significantly higher than GAAP ROIC.

Comparing against the average retail company demonstrated that Amazon’s 39x PE was only 2.6x the valuation multiple of the average company. Meanwhile Amazon’s ROIC was almost 9X the average ROIC, and Amazon’s earnings growth was 6-7x the average company’s earnings growth.

Looking at it from this perspective, on a relative basis, Amazon didn’t seem expensive.

Would that have been sufficient for you to buy Amazon in 2012? It’s an interesting question to ponder.

Take a moment to internalize the above slide.

Josh thought Amazon’s stock price would likely track Amazon’s revenue growth. His estimate: 30%/yr.

Remember, Amazon was already a $100 Billion dollar market cap company. And he was saying that Amazon would be worth $1.4 Trillion in 10 years!

#RealTalk: How would you have reacted had you heard him say that?

How did his Predictions Play Out?

Josh was spot on about what eCommerce penetration would be in 10 years: eCommerce penetration was 21.2% in 2022.

Amazon grew revenues at around 23.5% (including AWS) from 2012 to 2022. He was off by ~6.5% per year.

Amazon’s market cap ended 2022 at around $880 Billion, so just shy of a trillion dollars.

He was spot on about Amazon’s stock CAGR tracking its revenue growth: Amazon’s stock CAGR was ~24%.

Simply amazing.

Some Takeaways

This stock pitch was a work of art, a complete masterpiece in my opinion.

It’s an interesting thought exercise to ask yourself whether you would have bought the stock had you come across this writeup in 2012.

Here are some of my high-level takeaways:

Just because a company is large doesn’t mean it can't be a great investment. It’s not necessary to only invest in tiny or obscure companies to get a good return.

Betting on the leading player in a large and growing market can be very lucrative.

Mature businesses a company is disrupting may provide useful comps for how the company may look like at steady state.

Mean reversion is the norm, but if you can make a logical justification for when it is unlikely, that can be a very profitable exercise.

GAAP metrics are not always the best representation of the economics of a business. Adjustments to financial statements can create great clarity, and also provide a great way to better compare businesses in the same industry.

Marrying quantitative analysis with qualitative analysis can help build stronger conviction.

It’s interesting there was no mention of AWS, and how it would impact the future of Amazon. That clearly was an important value driver. I believe AWS revenue was only a couple of billion at that point (compared to ~$60B for the whole company), so inconsequential at the time.

Josh’s comments on “habits” provide some interesting mental models to keep in mind:

Repetition creates habit.

Intuition and behavior are influenced by habit.

Habits die slowly, but ultimately people respond to incentives.

Pay attention to facts that disagree with your intuitions.

This one in particular is interesting and something i need to think more about…for example, the recent rise of delivery businesses are a head scratcher for me.

What are the best stock pitches you have ever read?

If you send me one or a few that you’re most fond of, I volunteer to compile the best ones into a PDF and share it with you.

I think it would be a great way to crowdsource a valuable resource like this together, one that we can all learn from.

Please send them over.

Thanks!

If you’re new here, I am a fan of the Coffee Can Portfolio, an “Active Passive” approach to investing. The idea of a Coffee Can is simple: Buy a basket of the best stocks you can and let them sit for years. You incur no costs with such a portfolio, and it is simple to manage.

Coffee Can Next, Results To Date:

If you’ve been following along, we’ve now finished creating our coffee can:

Great article, thanks.

But I think it is important to mention, that he was also very lucky that AWS played out the way it did. He probably did not paid attention to it, because he underestimated its significance for the future (understandable, who would not have in 2012). Yet only with retail, Amazon's market cap would be significantly lower. Still probably a good investment, but with lower returns.