Studying Winning Stocks: Analyzing Costco (COST) in 2005

Can You Spot a 10-Bagger?

I am a fan of the Coffee Can Portfolio, an “Active Passive” approach to investing. The idea is simple: You try to buy a basket of the best stocks you can and let them sit for years. You incur no costs with such a portfolio, and it is simple to manage.

You can track my stock baskets here on my Scorecard.

In November, I shared Nicholas Sleep’s thoughts on Costco from June 2005. Including reinvested dividends, this stock has been a 10-Bagger since 2005!

You didn’t even need to come up with the investment idea. But if the thesis made sense to you, you could have made 10 times your money.

How Could We Have Evaluated The Investment Opportunity in 2005?

Of course hindsight is 20-20 but could we have developed the conviction to buy the stock had we come across the investment writeup in 2005?

Lets reverse engineer what Nicholas Sleep may have been thinking back then.

One framework to help us evaluate the investment opportunity is to answer the following questions:

Do I understand the Business?

Does the business have a durable competitive advantage?

Is the company management talented and can they be trusted?

Can I buy the business for a reasonable Price?

Let’s start.

1) Do I understand the Business?

In 2005, Costco was already a well-known retailer with a unique operating model. Unlike other retailers, a membership was required to be able to shop there. And according to Sleep, not only did Costco provide consumers better products (than the competition), but also better prices. Sleep pointed out that even Walmart (known for its low prices) had higher price markups than Costco.

Retailers are relatively straightforward to understand. They source or manufacture products, and sell those within their storefronts, or online. The beautiful thing about retailers is that their businesses are readily accessible to anyone. Although supply-side logistics complexity may be harder to evaluate, anyone can walk into a store and assess the company’s products quite easily.

As a result, verifying Sleep’s claim that Costco offered “better products at better prices” could have easily been done with a little bit of leg work, some shopping, and by casually interviewing Costco customers (not hard to find).

I’d say one could have understood the business relatively well.

So far so good.

2) On Competitive Advantage

Nicholas argued that Costco’s competitive advantage came from the following sources:

The real power of Costco’s strategy – and the source of its competitive advantage, according to Sleep – is how the benefits of growth are reinvested in the relationship with the consumer. As Costco opens new stores, supplier and other scale cost savings are passed back to customers through even more competitive prices. Customers then respond to the better prices, driving incremental revenue at both new and old stores.

As Sleep writes: “In the office we have a white board on which we’ve listed the very few investment models that work and that we can understand. Costco is the best example we can find of one of them: scale efficiencies shared with customers. We often ask companies what they would do with windfall profits, and almost no one replies ‘give it back to customers’. How would that go down with Wall Street? That is why competing with Costco is so hard to do. The firm is not interested in today’s static assessment of performance. It is managing the business to raise the probability of long-term success.”

What the above is saying is that Costco, because of its scale, had a cost advantage. As a result, it had more margin than its competitors to play with. Therefore, it had the flexibility to deploy that margin into its customer value proposition by lowering prices, or by increasing its service or product quality. As a result, by improving its customer value proposition, Costco could further increase customer loyalty and spend, grow market share, and be in an even more advantaged position. This was a self reinforcing flywheel.

This flywheel advantage was not obvious at the time and likely not as well understood as it is today. Sleep refers to this flywheel as “scale efficiencies shared”. It is this key insight that was at the heart of Sleep’s investment thesis, and it is the major idea that investors needed to buy into, to truly internalize Costco’s durable competitive advantage. Without this belief, Costco would not have looked like a superior competitively advantaged company… it had extremely low margins (less than 2% after tax)!

A Quick Detour: Investing Knowledge Compounds

It’s interesting how investment knowledge compounds over time, and how patterns re-emerge. Sleep certainly took advantage of this.

Several years ago, Sleep invested 30% of his portfolio into Amazon (AMZN), a massive high-conviction bet. He did so because of the clear similarities he saw between Costco and Amazon’s business models. For example:

Like Costco, Amazon’s business was structurally advantaged (compared to brick and mortar retailers).

The Amazon Prime Fee was similar to Costco’s Membership Fee, which created customer loyalty and increased spend, not to mention subsidized products and deliveries.

All the Prime benefits are examples of Amazon using it’s extra margin to improve its customer value proposition by increasing its service & product offerings.

Here’s what Amazon had to say about “scale efficiencies shared”:

“As our shareholders know, we have made a decision to continuously and significantly lower prices for customers year after year as our efficiency and scale make it possible.

This is an example of a very important decision that cannot be made in a math-based way. In fact, when we lower prices, we go against the math that we can do, which always says that the smart move is to raise prices. We have significant data related to price elasticity. With fair accuracy, we can predict that a price reduction of a certain percentage will result in an increase in units sold of a certain percentage. With rare exceptions, the volume increase in the short-term is never enough to pay for the price decease. However, our quantitative understanding of elasticity is short-term. We can estimate what a price reduction will do this week and this quarter. But we cannot numerically estimate the effect that consistently lowering prices will have on our business over five years or ten years.

Our judgment is that relentlessly returning efficiency improvements and scale economies to customers in the form of lower prices creates a virtuous cycle that leads over the long-term to a much larger dollar amount of free cash flow, and thereby to a much more valuable Amazon.com. We have made similar judgments around Free Super Saver Shipping and Amazon Prime, both of which are expensive in the short term and – we believe – important and valuable in the long term.”

3) On Management Talent & Integrity

In 2005, the management team at Costco already had a great reputation. Investors believed that the company was very focused on the creation of long-term value and delighting its customers. That said, many investment analysts believed that employees and customers were unduly rewarded to the detriment of shareholders.

I find this type of reasoning quite odd...Costco was already a very successful business at the time. Throughout its history, it had rewarded its customers and employees just like it was doing in 2005. So of course, its shareholders had benefited from this practice. At the risk of falling victim to survivorship bias, I believe rewarding its customers and employees was a necessary component of Costco’s success...I imagine this line of analyst thinking is yet another example of Wall street’s focus on short term profits.

Anyway, in 2005, James Sinegal, CEO of Costco was extremely well regarded and considered to be “the architect behind Costco’s unique and disciplined culture”. But he was almost 70, so Senegal’s future departure from the company was inevitable.

As a result, the questions we’d have had to ask ourselves at the time were “Will Costco’s culture and competitive advantage endure after Senegal’s departure?” and “Will the company appoint a worthy successor?”

Nick was clearly comfortable answering “Yes” to both these questions. He was comfortable deferring to the Board.

As you can see, this was a judgement call.

Long-term shareholders often need to make this type of decision when Founding CEOs retire or leave a company. Many long-term Apple (AAPL) shareholders faced a similar decision when Steve Jobs stepped down. I imagine many Berkshire Hathaway (BRK) shareholders are faced with a similar decision today.

4) Can I Buy the Business For a Reasonable Price?

Costco traded at a ~24 P/E, but Sleep didn’t think this was expensive. He felt that Costco had lots of growth opportunities ahead, everything from store count growth, membership growth, geographic expansion, and more asset turns from even lower future prices. As a result, despite $50 Billion in annual sales, Sleep felt that Costco was still an early life-cycle company, and one whose competitive moat would get deeper as the company got bigger.

Let's look at these factors more closely.

Store Count:

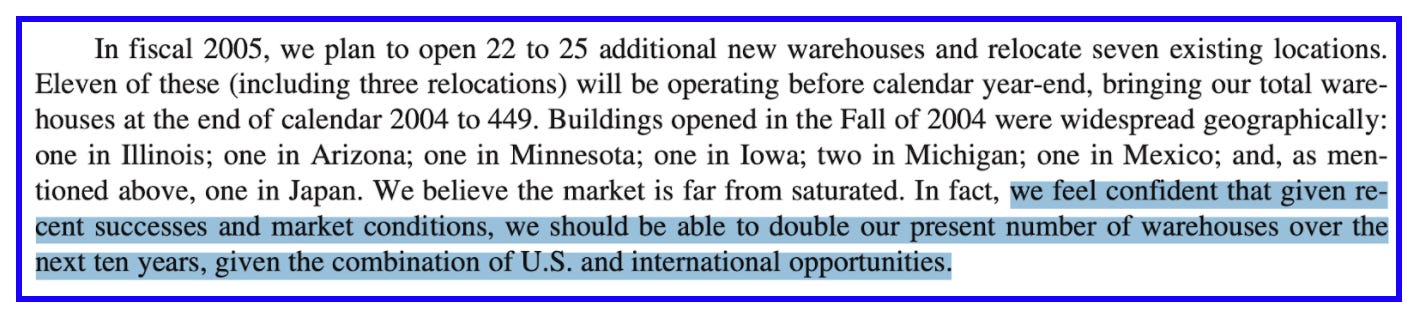

Excerpt from Costco’s 2004 Annual Report:

At the end of 2004, there were only 400+ warehouses in operation. Doesn’t seem saturated at all. That turned out to be the case. As of December 2020, Costco had 803 locations.

International Expansion:

Their international footprint today is just 245 stores:

Canada (102)

Mexico (39)

United Kingdom (29)

Japan (27)

Korea (16)

Taiwan (14)

Australia (12)

Spain (3)

Iceland (1)

France (1)

China (1)

Even today, it feels like there is ample room for international expansion. In 2005, this was even more so the case.

Membership Growth:

According to the writeup, in Seattle and Alaska, the penetration of membership cards was an astonishing 65% of households, but in most markets it was below 10%. This was the membership growth opportunity.

In 2004, Costco had ~15 million Gold Star members and ~5 million business members.

Since only 1/3 of the store base was in California, and almost half on the West Coast, it was not hard to imagine that membership would grow. That said, it likely wasn’t clear by how much. So the challenge must have been figuring out how much of this growth was (a) possible and (b) priced in.

Today, Costco has ~47 million Gold Star members (>3X) and ~11 million business members (>2X).

Asset Turns:

Would Costco experience increased asset turns?

We can see from the table below that Sales Per Warehouse were increasing every year, like clockwork (notice how the numbers in each row increase from left to right).

In fact, we could also see that mature stores continued to grow sales per warehouse at a very healthy clip. For example, the most recent 2-year growth rates at the 2 oldest cohorts were 19.51% (stores opened in 1996) and 12.61% (stores opened in 1995 or earlier) respectively. Not bad for stores that were already 10 years old!

We could also see that newer stores grew sales per warehouse at much higher rates than those of mature stores. For example, the most recent 2-year growth rates at the 2 newest cohorts were 32.76% (stores opened in 2002) and 33.33% (stores opened in 2001) respectively.

I haven’t done a very thorough analysis of the numbers here but both of the above demonstrated strong return on incremental invested capital and were important aspects of Nick’s thesis.

Nicholas Sleep indeed saw the future. This is what the data looks like for the last 10 years. Still growing…like clockwork.

eCommerce:

I don’t believe there was any mention of eCommerce in Sleep’s thesis but this clearly represented a growth opportunity for Costco. In 2004, the company believed that eCommerce would be a $5 Billion business in the next several years. By comparison, in 2020, Costco eCommerce did almost $10 Billion in sales!

By analyzing the above 5 growth opportunities, we could have figured out relatively quickly that Nick’s assertion that Costco was still an early life-cycle company was indeed a legitimate claim.

That said, to have followed through with an investment, one had to believe that the company's future growth prospects were not fully baked into the company’s market value. This required valuing the company. Of course valuation is more art than science so, as always, one would need to make their own growth assumptions and come to their own conclusions.

Wrapping Up

Costco (COST) turned out to be a great winner... and it may still have room to go. But, it wasn’t an easy stock to hold on to. If you had invested in 2005, you’d be down 10% after four long years, primarily because of the financial crisis.

But if you understood Costco’s competitive position, and also had a long investment horizon, this could have been a buying opportunity. Why? Because the worse the economy gets, the better it is for Costco’s competitive position because of their cost advantage. Sales were down only ~3% in 2009, earnings about 15%, but the stock significantly more so earlier in the year.

Of course, this is easier said in hindsight. The financial crisis would have certainly tested one’s patience and conviction.

Would you have bought this stock in 2005 had you come across this writeup?

If you enjoyed this article, share it with a friend. They may like it too!