Is Wolfspeed the next Carvana (up 98X) or Rolls-Royce (up 19X)?

When Good Companies Hit Debt Trouble, Smart Money Gets Rich

If you like this article, please do share it with a friend & click the ❤️ . Thanks :)

If you’re new here, I share “buy-and-hold portfolios” that can double in 3-5 years. Our investment philosophy is simple: Try to find the best stocks you can and let them sit for years. Incur no costs with such a portfolio, and it is simple to manage.

Here is the performance of our current active portfolios (zoom in):

Past Portfolio Performance:

Playing For Doubles Alerts

I’ve been sending free same-day notifications of my buys/sells to folks on the Playing For Doubles Alerts Waitlist.

For those who’ve signed up, I hope you’ve benefited from this. I especially hope it was helpful to see how we built Portfolio 14 during the high-volatility drawdown period following the tariff announcements on April 2.

If you’re interested in receiving these alerts, join the waitlist here.

Good Companies + Debt Problem = Multi-bagger Opportunity

Picture this: You're walking through a garage sale and spot what looks like a genuine Rolex buried under a pile of costume jewelry, priced at $20. The seller, clearly unaware of what they have, just wants it gone. That's exactly what happens in the stock market when fundamentally strong companies hit temporary debt troubles.

While most investors flee at the first whiff of financial distress, savvy contrarians see something entirely different: the setup for potential multi-baggers.

Today, we're diving deep into one of my favorite investment patterns, what I call the "Good Company + Debt Problem". It's where diamonds hide in the rough, waiting for patient investors who can see beyond the balance sheet scare stories to the underlying business strength.

This isn't about catching falling knives or gambling on turnarounds. It's about identifying world-class companies temporarily knocked down by solvable problems, then positioning yourself for the inevitable rebound.

Let me show you how this pattern has created some of the most spectacular returns in recent memory.

The Investment Pattern

The "Good Company + Debt Problem" pattern rests on a simple but powerful premise: exceptional businesses with temporary financial issues often get thrown out with the genuine bankruptcy trash. The key word here is temporary.

What makes a "good company" in this context? Ideally, we're looking for market leaders with durable competitive advantages operating in secular growth industries, what Warren Buffett would call, “companies with moats." These companies have proven they can generate cash; they just hit a rough patch that strained their balance sheets.

The debt problem creates the opportunity. When leverage ratios spike and credit markets tighten, fear takes over. Institutional investors bound by risk mandates dump shares. Retail investors, spooked by bankruptcy headlines, head for the exits. Short sellers pile on. The result? A temporarily dislocated stock price that bears no resemblance to the underlying business value.

Here's where psychology meets opportunity: humans are wired to extrapolate current trends indefinitely. When things look bad, we assume they'll stay bad forever. But great investments can often come from betting against this cognitive bias. When everyone else sees death spirals, contrarians see reset buttons.

The criteria for identifying recovery candidates are specific:

Dominant market position

Secular growth tailwinds

Management with a clear path to debt resolution (i.e the future catalyst)

Example 1 Rolls-Royce (RYCEY): A 19-Bagger since September 2022

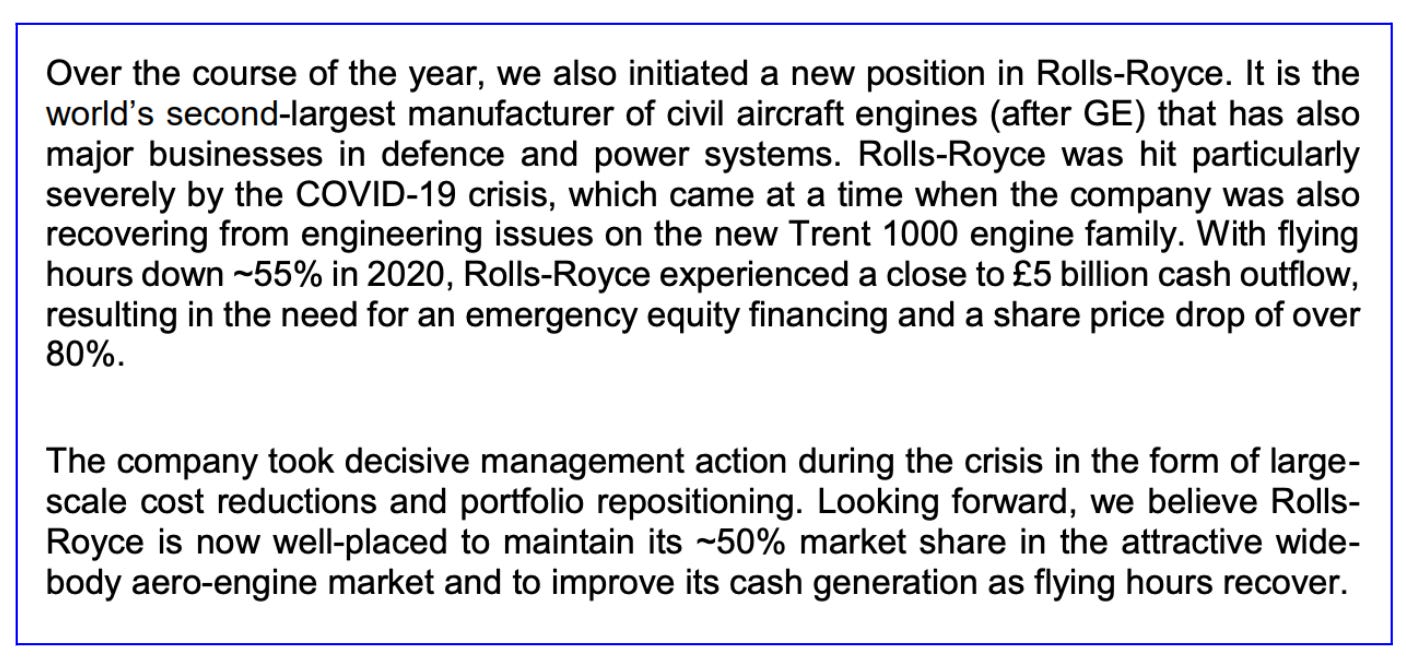

Let me tell you the story of one of the most spectacular turnarounds in recent market history. Rolls-Royce wasn't just any company facing debt problems, it was the crown jewel of British engineering, maker of some of the world's most sophisticated aircraft engines, suddenly staring into the abyss.

Pre-COVID, Rolls-Royce looked unstoppable. The company had transformed from a cyclical manufacturer into a services powerhouse, with 60% of revenues coming from long-term maintenance contracts. When you sell an engine to Boeing or Airbus, you're really selling decades of high-margin aftermarket services, a beautiful recurring revenue model with high returns on capital.

Then came March 2020. Global aviation ground to a halt virtually overnight. Rolls-Royce's "Power by the Hour" contracts, where airlines pay based on flight hours, meant revenue collapsed alongside air travel. The company that had generated >$1 billion in free cash flow in 2019 suddenly faced significant annual cash burn.

By October 2020, shares hit as low as $1.38/share (Ticker $RYCEY). The company was burning through billions, had significant debt, and bankruptcy whispers grew louder. Most investors saw a dead man walking. But here's what the sellers missed: the underlying business hadn't changed. Their Trent engines still had significant market share, and the longterm secular growth in air travel, driven by emerging market middle classes, remained intact.

The turning point came when EXOR, the Agnelli family's investment vehicle, stepped in with a large investment in the company. Here is what they said about the opportunity:

They recognized that air travel would recover, and when it did, Rolls-Royce would mint money again.

The recovery metrics tell the story:

Air travel passenger miles have now exceeded pre-COVID levels.

Rolls-Royce generated almost $3 Billion in free cash flow in 2024,

Debt has dropped, and the stock trades around $13 today, a 19X gain from the lows. ($0.71/share).

I was lucky enough to buy the stock with an average price of $1.49/share. Although it dropped ~52% in 2022, it is now up almost 9X.

This should help demonstrate the power of this investment pattern.

Example 2 Carvana (CVNA): A 98-Bagger since December 2022

Free Download")

If Rolls-Royce was about patience during a global crisis, Carvana's story is about recognizing disruption hiding behind debt drama. This is the "Amazon of car sales", a company that took one of the most painful consumer experiences (buying a used car) and made it as easy as ordering a book online.

Carvana's pre-crisis story was compelling: car vending machines, 7-day return policies, and a vertically integrated model that eliminated dealer negotiations and markups. The founder Ryan Keeton looked like a visionary.

Then came the perfect storm. Rising interest rates and inflation lessened car demand. Carvana's rapid expansion, funded by debt, suddenly looked reckless. A major contributing factor to their debt increase was Carvana's $2.2 billion debt-funded acquisition of ADESA's U.S. auction business. This deal closed in May 2022. By December 2022, shares hit $3.55, down 99% from the peak. Bankruptcy seemed inevitable.

But here's what the market missed: Despite the chaos, Carvana was gaining market share even as overall used car sales declined. Management was aggressively cutting costs, reducing inventory, and, crucially, negotiating debt restructuring deals.

The catalyst came in early 2023 when Carvana successfully refinanced billions in debt, extended maturities and reduced cash interest payments. Suddenly, the company had breathing room. Used car demand began recovering as interest rates stabilized. Carvana's online-first model looked prescient as traditional dealers struggled with changing consumer preferences.

The numbers speak for themselves:

From that $3.55 low, shares rocketed to $348 by November 2024—a 9,700% gain.

The company returned to positive free cash flow, inventory turns improved, and they're now expanding internationally.

What looked like a debt-fueled collapse was actually a temporary mismatch between growth investments and market conditions.

Unfortunately, I missed this one… 🙁

Current Opportunity, Wolfspeed (WOLF)?

Now let's examine what might be our next case study unfolding in real-time: Wolfspeed, the semiconductor company sitting at the intersection of two massive secular trends, electric vehicles and renewable energy.

Wolfspeed makes silicon carbide semiconductors, the chips that make EVs charge faster and renewable energy systems more efficient. These aren't commodity chips; they're specialized products with 10x better performance than traditional silicon in high-power applications. The company holds over 3,000 patents and supplies Tesla, Mercedes, and other automotive leaders.

The opportunity is massive. The silicon carbide market is projected to grow from $1.5 billion today to $8 billion by 2030, driven by EV adoption and grid modernization. Wolfspeed is building the industry's largest manufacturing facility in North Carolina, positioning for this boom.

But here's the challenge: building semiconductor fabs requires enormous upfront capital. Wolfspeed has burned through billions in cash, debt has risen to $6.2 billion, and the stock has fallen 99% from its 2021 highs.

Sound familiar?

The parallel to our previous examples is striking:

Like Rolls-Royce, Wolfspeed provides a critical technology to a secular growth industry.

Like Carvana, Wolfspeed is investing heavily in capacity just as end markets face temporary headwinds.

The question is whether this represents the same opportunity pattern we've seen before…

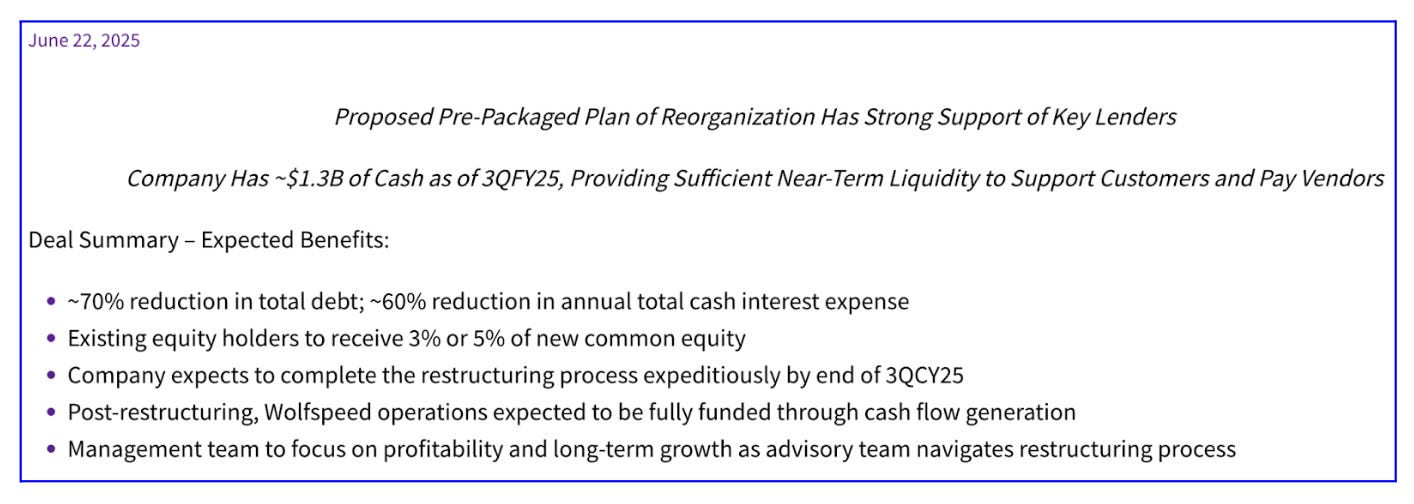

It was interesting that they announced a debt restructuring plan on June 22 (the catalyst):

But, this caused the stock to drop around 30% to around 65 cents per share.

A few days later, the Company voluntarily filed petitions for reorganization under Chapter 11 of the U.S. Bankruptcy Code. The stock bottomed at 39c per share, and in just 3 days tripled. It closed at $1.18/share on Thursday July 3.

Some Napkin Math:

At 65 cents per share, the day after the debt restructuring announcement, the stock was valued ~$100 million.

At 39 cents per share, at the bottom, the stock was valued at ~$60 million.

According to CEO Gregg Lowe, the company targets its 200mm silicon carbide facilities at Mohawk Valley and North Carolina to generate approximately $3 billion in revenue annually when fully operational, with > 40% EBITDA margins at full capacity.

Current debt is ~$6.2 Billion. With the 70% reduction via restructuring, we get $1.86B.

If we believe these numbers, and say it takes ~5 years for them to reach that milestone, in 5 years we get an enterprise with <2B of debt, $10-12B of market cap (assume 8-10x EBITDA multiple), plus any cash.

If existing equity holders are receiving 3-5% of new common equity, that could be worth say $300-$500 million at a $10B market cap. Add to this some good news in the coming years, and we could witness an investment homerun.

No wonder the stock tripled in 3 days.

Do You See Opportunity Here?

As we watch Wolfspeed's story unfold, I'm curious about your perspective. Do you see an opportunity here? I’d love to hear your analysis.

If you’re familiar with the company, the situation, or the silicon carbine value chain, I’d love to speak with you. Do please get in touch.

If you’re not familiar with the above, but would like to learn what I might fight out, please leave a comment below. If I end up hearing from anyone, I will let you know.

If you liked this article, please do share it with a friend & click the ❤️ . Thanks :)

Related Articles:

Another Q: if they succeed in chapter 11 proceedings will the share count be impacted? If I bought 100 shares today @$2 but once re-org happens I am left with 3 shares then it will be a losing game?

There is definitely an opportunity here, but upon researching the difference here:

1. WOLF was never a good executor compared to the other two examples here. Also, there is a lot of competition vs almost no competition for RR and Carvana

2. Huge capacity coming online from competitors, and also huge pressure from China(Tariff can help here)

3. They started shipping Sic in 2023, but still not huge growth

I am not able to attach a screenshot, but will share notes here

https://www.perplexity.ai/search/can-you-give-me-a-table-of-sum-rMYKJKq9RpiO4OYyLIgxnQ#4