Investing Homeruns

How big do they need to be?

We live in an uncertain world and therefore, it would be foolish to expect all investments to be profitable. To account for losses in our portfolio, in order to make money, we must find an investment strategy that has a positive expected return.

Expected Return =

Probability(Gain)*(Avg Gain) + Probability(Loss)*(Avg Loss)

What’s the Expected Return for Investing in Mavericks?

To be successful, I believe the returns distribution of the Investing in Mavericks strategy needs to be similar to that of a good Venture Capital Portfolio.

A good VC portfolio tends to generate the following returns distribution:

30-40% Distractions (VCs experience a 100% loss)

30-40% Base Hits (VCs experience a small loss or gain)

10-20% Homeruns (VCs experience outsized gains to make up for all the Base Hits and Distractions)

Therefore,

Expected Return =

Probability(Homerun)*(Avg Gain) +

Probability(Base Hit)*(Avg Gain) +

Probability(Distraction)*(Avg Loss)

How Big do the Homeruns need to be?

Let’s assume the following:

A $1,000,000.00 portfolio.

An investment approach where we simply make 10 equal investments of $100,000.00 (10% each).

A 10 Year Time Horizon.

An expected +100% market return during this time (~7%/yr).

Therefore, in order to beat the market, our expected return needs to be > 100% over this 10 year period.

Let’s walk through a few scenarios.

Case 1: The VC Equivalent

If our results followed the returns distributions of a typical good VC portfolio, we would expect the following:

40% (4 companies) to lose 100% of our investment.

40% (4 companies) to breakeven.

20% (2 companies) to carry our portfolio forward.

We would require an 8X on the $200,000 invested in just two of the companies to match the market’s return over 10 years. No small feat.

What Can we do to Improve our results?

We have three variables to play with:

Maximize the Homeruns

Minimize the Distractions

Improve the Base Hits

Case 2: Smaller Distractions

Although I view Investing in Mavericks to be like deploying Venture Capital in the Stock Market, there are big differences between investing in Public companies vs investing in unproven startups.

As a group, Public companies are significantly less risky compared to startups. A company must pass a significant gauntlet in order to go Public. They must recruit a team, find product market fit, develop a sound business model, raise money from credible private market investors, and demonstrate many years of operating history, not to mention actually go through the heavily scrutinized IPO process. This is not easy. Just look at what happened to WeWork.

As a result, unless one ends up investing in a fraudulent company, I’m willing to argue that losing 100% on our underperforming investments is unlikely (assuming zero leverage).

As a result, I’d expect the downside of our Distractions to be significantly better than that of a VC portfolio.

Therefore, if we manage to limit the losses on our Distractions to say, 50%, that means our Homeruns now need to produce a 7-Bagger, not an 8-Bagger. A slight improvement to Case (1).

Although we can try to further limit our losses from Distractions, we know that all Mavericks start out as Disruptors, and their success isn’t at all guaranteed. I believe that investing in Distractions is a necessary requirement in order to ultimately invest in the Homeruns. So we should always expect Distractions in our portfolio.

Case 3: Better Base Hits

But what about Base Hits? I think we have more flexibility there.

Remember, when investing in Mavericks, we are investing in companies that have the potential to become the greatest companies of our time. Add to that the fact that we expect to invest in a rising market over time. So why can’t we expect our Base Hits to match the return of the market?

I expect some Base Hits to underperform (but nowhere near as badly as the Distractions), but I also expect some Base Hits to beat the market, just not by so much that they’d be considered Homeruns.

I don't believe this to be an unreasonable assumption. As a result, unlike in Venture Capital, I think the right comparison baseline for Base Hits is not “breakeven”, it is the market return.

If our Base Hits match the market, we require our Homeruns to produce a 6-Bagger.

Case 4: Better Base Hits AND Smaller Distractions

Combining Case (2) and (3) gives us the following.

In this case, we require our Homeruns to produce a 5-Bagger.

Can we do Better?

If we can realize the above optimizations, our Homeruns need to produce a 5-Bagger instead of an 8-Bagger. That is a significant improvement.

But, can we do better?

Case 5: Improving the Base Hits

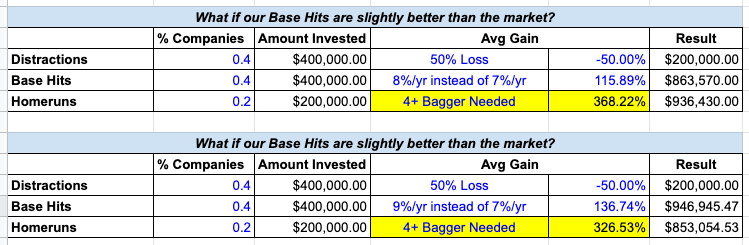

I argued earlier that it is not unreasonable to expect our Base Hits to match the return of the market. But if we can squeeze just a little more juice out of these Base Hits, and beat the market by 1% or 2% per year, then we would need slightly more than a 4-Bagger from our Homeruns to match the market’s return.

Not easy but not impossible.

Case 6: Reducing Distractions AND Increasing the Base Hits

So far, we have assumed a 40-40-20 return distribution. What if we can improve our hit-rate? That is, what if we can reduce our Distractions slightly and instead increase our Base Hits a bit?

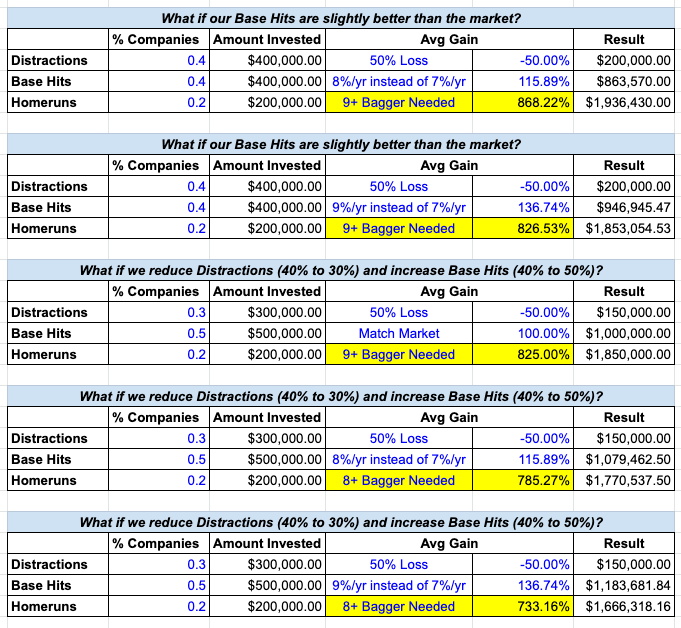

This can dramatically reduce the magnitude of the Homeruns needed. Below, I have used a 30-50-20 return distribution to demonstrate.

This is very hard. Improving our hit-rate requires a dangerous tradeoff. If we try too hard to minimize our Distractions, we may not be taking enough risk to hit the Homeruns. This can result in mediocre returns. This happens to underperforming Venture Capital firms all the time.

What if we wanted to Double the Market’s Return?

To do this, we would need to aim for a triple (+200%) in 10 years, instead of the above double (+100%).

As you can see from the below, with the above simplistic investment approach, it is significantly harder to triple our capital versus doubling it.

Even Case (6) below requires our Homeruns to be 8-9 Baggers!

A Better Investment Approach

Relying on a 8+ Bagger AND needing our Base Hits to beat the market seems quite hard. As a result, the above approach of simply investing 10% in 10 companies may not be the best approach. Instead, we must strive to invest more of our capital into the Homeruns, as they emerge, and as little as possible into the Distractions and Base Hits, relatively speaking.

This is difficult for two reasons:

First, this requires us to invest more at higher prices. This is psychologically difficult. But this is exactly what good VCs do: buy more of the companies that truly breakout from the rest.

Second, unlike VCs who typically have controlling interests in the companies they invest in, we, as public market investors, have much less information with which to make our investment decisions.

With that said, investors who are able to buy more of the right breakout companies, can differentiate their portfolios and significantly outperform.

As you can probably tell, the above is not easy. But that is exactly what makes Investing in Mavericks the most interesting, fun, and intellectually challenging endeavor I have ever come across.

To continue learning how to Invest Like a VC in the Stock Market, Subscribe.