The Hidden Math of Portfolio Success

The Importance of Building A Winning Team

If you like this article, please do share it with a friend & click the ❤️ above. Thanks :)

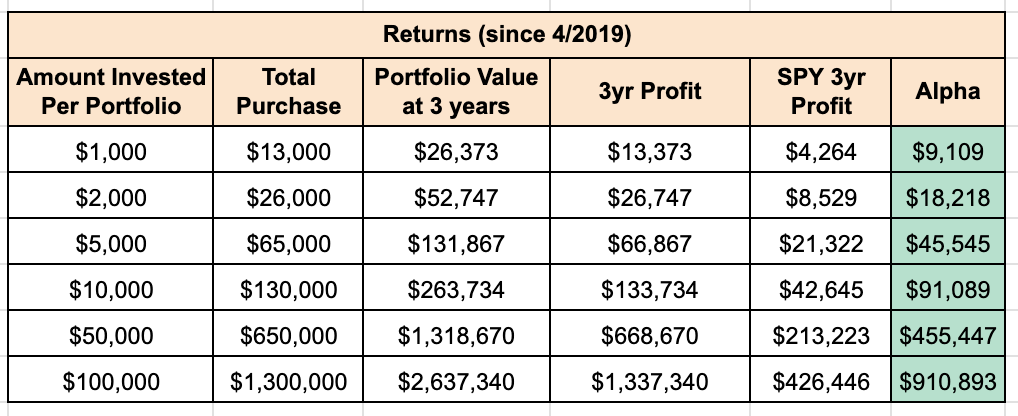

If you’re new here, I share “buy-and-hold portfolios” that I believe can double in 3-5 years. Here is the performance of our 2 current active portfolios:

An equal amount invested in each portfolio would have returned the following:

You can track my Live Investment Scorecard here.

Next portfolio starting in January 2025.

To receive timely notifications of my buys/sells, join the waitlist here

The Hidden Math of Portfolio Success

The 1989 Minnesota Vikings made a costly mistake: Trading eight draft picks for running back Herschel Walker, they banked everything on a single player. Meanwhile, the Dallas Cowboys used those picks to build a dynasty, winning three Super Bowls in the 1990s. This stark contrast offers a valuable lesson for portfolio management: success often comes from building a balanced team rather than betting everything on one superstar.

While the intensity of a concentrated portfolio can yield spectacular returns, it also breeds overthinking and significant vulnerability. One mistake can meaningfully drag returns, just as Walker's mediocre performance crippled the Vikings.

Although the allure of concentrated investing can be intoxicating, I believe that many concentrated investors, as they mature, especially those who have made mistakes, naturally expand their number of portfolio holdings. Despite these additional investments, such a portfolio can deliver similar returns with much less volatility compared to a hyper-concentrated approach.

Take, for example, the following returns, which one do you think results in the best outcome?

Portfolio 1: Hyper-Concentrated (say 3-4 stocks):

Year 1: +75%

Year 2: +30%

Year 3: -35%

Portfolio 2: Concentrated (say 5-15 stocks):

Year 1: +15%

Year 2: +18%

Year 3: -3%

Portfolio 3: Diversified (say 25+ stocks):

Year 1: +10%

Year 2: +10%

Year 3: +2%

Portfolio 3 results in +25.6% return after 3 years.

Portfolio 2 results in +43.1%.

Portfolio 1 results in +47.9%.

A hyper-concentrated portfolio of just a handful of stocks can generate massive returns but can also have huge swings and large drawdowns. Even the best performing stocks in history have had multiple drawdowns of >50%. Due to the geometric nature of compounding, such drawdowns can have a detrimental impact on total returns.

Notice how portfolio 2’s annual returns are nowhere near as “exciting” as portfolio 1’s but the net outcome is quite similar to that of portfolio 1.

Of course, I am cherry-picking numbers here to make my point…but you get the idea.

Core Holdings And The Farm Team

Investing requires us to bear uncertainty in the pursuit of attractive returns. This means we must build conviction. And building conviction in positions is very much like developing trust in relationships—it can't be rushed.

The highest conviction positions, like the most enduring relationships, develop organically over time. We can refer to such investments as “core holdings.” They are like veteran players on a team—they've proven themselves under pressure, earned their "playing time and compensation" and demonstrated reliable performance. As core holdings grow, they increasingly drive portfolio performance. We see this today in the S&P500, where the majority of performance is driven by a handful of the largest market cap companies.

But capitalism is brutal. Companies stall, change, fail, or go bankrupt all the time. So to complement the core holdings, successful portfolios can maintain a "farm team" of other bets: These are typically promising but less-proven investments. Like minor league prospects, they face constant evaluation. Strong performers earn promotions to core positions, while underachievers get cut.

When it comes to Investing in Mavericks, I sometimes view “Disruptors” and “Seed Investments” as the farm team, and Leaders as the core holdings.

“As Mavericks grow and evolve, they go through three stages of development. As they graduate from one stage to the next, they reduce risks inherent in their businesses. Naturally, this reduction in risk warrants higher valuations. Therefore, I believe that buying or increasing stakes in these businesses, when they have been further de-risked, can be a rewarding investment strategy.”

(See Portfolio Permutations):

“Venture Capital is a lot like Poker (Texas Hold’em). A seed Investment is like “the ante.” It is like buying an option to “see the cards” and play in the next round. After investing, investors learn in greater detail how the management team operates, they learn the nuances of the market the company is operating in, they observe the strengths and weaknesses of the competition etc. Then at that point, investors can decide whether they want to see "the flop", that is, do they want to pay to see how the company performs in their next phase of growth. The price to see this is usually higher. If they don’t like their cards, they can fold. They can cut their losses. They can preserve their capital and wait for the next deal.”

The Math of Concentration Risk

The mathematics of concentration risk are sobering.

Consider a portfolio where a 40% bet suffers a 30% decline. This creates a 12% drag on the total portfolio. To offset this single loss, you'd need multiple large wins from your smaller bets. For instance, two 6% bets would each need to gain 100% just to breakeven. This math illustrates why even a few missteps in concentrated positions can require herculean efforts from the rest of the portfolio.

That is, when your “superstars underperform,” the rest of the team must excel to compensate.

The Venture Capital Way

The path to good returns is complicated. On the one hand, the Pareto Principle states that 80% of our returns will likely come from 20% of our bets. So why not try and identify the 20%? I suppose that sounds good in theory, but everyone makes mistakes, so this is quite hard to do in practice.

As Einstein said:

“In theory, theory and practice are the same. In practice, they are not.”

This is where the Power Law can come in. If our portfolio exhibits venture capital-like power law dynamics, the best investment ends up being worth more than all the rest of the investments combined.

I prefer attempting to construct portfolios where I could benefit from such power-law dynamics. This is what Investing in Mavericks is all about.

Using this strategy, we are trying to construct a portfolio where we:

Take enough risk in our holdings such that upside potential is high, AND

Diversify sufficiently (but not excessively), AND

Hold on to our investments long enough, such that we can get outsized returns from a handful of our bets.

This is the Venture Capital Way.

If we are successful, the winners (which should return multiples of their original investment) should cover the losses from all the mistakes, and then some...

As a result, in investing, like in sports, building a balanced well-constructed team (i.e. portfolio) often trumps relying on individual superstars.

In Conclusion

Howard Marks said: “I believe most strongly that… the best foundation for above-average long-term performance is an absence of disasters.”

So, how do we avoid disasters?

Only take risks:

We’re aware of (i.e. do our research and analysis, and build conviction)

We can diversify (i.e. pick a good investment / portfolio construction strategy)

We’re well paid to assume (i.e. only make “High upside, low downside” bets)

One way to do this is The Venture Capital Way.

If you liked this article, please do share it with a friend & click the ❤️. Thanks :)