TEVA: A Highly Asymmetric Bet?

I am a fan of the Coffee Can Portfolio, an “Active Passive” approach to investing.

The idea is simple: Try to buy a basket of the best stocks you can and let them sit for years. You incur no costs with such a portfolio, and it is simple to manage.

You can follow and track my stock baskets here, on my Performance Scorecard.

❤ If you enjoy this post, throw it a like by clicking the heart up top to help more people find it.

“History doesn’t repeat itself but it often rhymes.”

--Mark Twain

Last week, I wrote about Jamie Mai of Cornwall Capital, and his unique propensity to identify highly asymmetric trades, which resulted in 40X returns in 9 years!

We discussed an example from 2003, where Altria, the cigarette maker’s market cap had been cut in half because of several large class action lawsuits underway at the time. Mai felt that as uncertainty about the lawsuits dissipated, it would either validate concerns about the litigation, in which case, the stock price would sell off substantially, or the reverse, in which case, the stock would appreciate materially. In other words, Mai felt that this situation would result in a bimodal outcome.

Mai placed a trade that made him 2.5X his money in relatively short order (although he lamented that he sold too soon).

Why is that interesting? Well, Teva Pharmaceuticals (Ticker: TEVA) today, finds itself in an eerily similar situation to that of Altria back in 2003.

Can we devise a trade with TEVA just like Mai did?

Let’s explore a little further.

What’s The Setup?

TEVA is a 120 year old Global Pharmaceutical company, with a $10 Billion Market Cap. TEVA stock however is down almost 90% since 2015.

Although the business has been affected by lower revenues & earnings, and increased leverage, Teva is now a legal liability story. Teva trades at a whopping ~25% earnings yield because it faces significant litigation, including price fixing lawsuits and opioid liabilities.

What Caught My Eye?

This feels like Altria in 2003, a situation where if we look forward a few years, it is unlikely that Teva’s share price will still be trading at the current ~$10 level as its legal liabilities become clearer. Positive litigation news (or news that isn’t as bad as expected) should lead to a material increase in the stock price, while negative litigation news could tank the stock even further.

The Poor Man’s Research

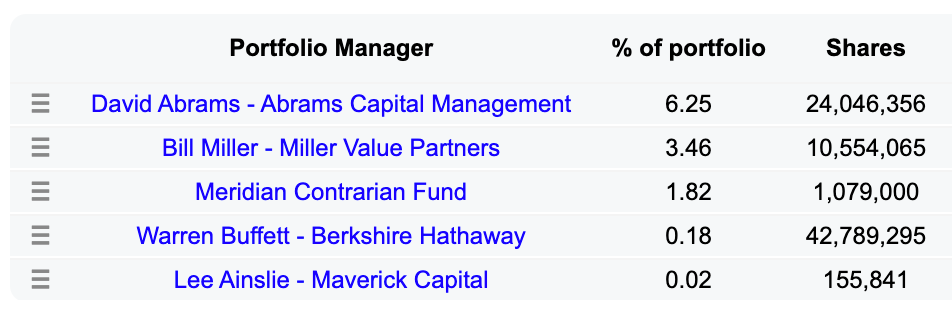

Several prominent and respected value investors own the stock.

These are all shrewd investors who pay particular attention to downside risk before making an investment. The fact that they own the stock gives me some comfort that the company has a good likelihood of remaining a going concern. Therefore, the downside scenario doesn’t interest me. The real asymmetric outcome would come if the stock price substantially increases from $10.

Bill Miller, a renowned investor, sees the same opportunity:

In November 2020, Bill said that he doesn’t expect the opioid settlement to be more than $1 Billion, and believes shares could rise to $25-$30 once the legal issues pass.

On June 14, 2021, his firm said: “While we appreciate the market’s concern regarding a large liability, history has shown that these settlements end up being at levels significantly lower than market fears.”

So, What’s The Trade?

First, Pharma litigation is outside my circle of competence. It’s hard therefore to game theorize potential outcomes. So this opportunity is perhaps best suited for someone who is closer to the Pharma industry, or someone with the time to better understand the lawsuits currently underway.

Otherwise, without further diligence, to place a trade, one would need to trust the above setup, and be willing to clone the investors listed above. Perhaps, shameless cloning can lead us to financial success?

If one can get comfortable with the above hurdle, the second challenge is finding the right trade. We have two choices:

The safest approach is to just buy the stock, like the investors above.

A riskier approach is to buy Call Options, like the ones Mai used. Although riskier, this can create a highly asymmetric bet. Let’s take a closer look.

Which Call Options Could We Choose?

This is an art.

Choosing an option requires both, selecting a strike price and an expiration date.

If you’re new to Options, see:

Recall that a Call is simply a contract that gives you the right to buy 100 shares of a stock for a specific price (i.e. the Strike Price) by a certain date (option expiry date).

If one believes that the upside in TEVA stock is indeed a $25-$30 stock price, we have a few choices:

Buying In the Money Calls (i.e. calls with a strike price below $10) can provide us some leverage. The lower the strike, the lower the leverage.

Buying Out the Money Calls (i.e. calls with a strike price above $10) can provide us significantly more embedded leverage. The higher the strike, the higher the leverage.

Selecting the expiration date is harder.

The catalyst here is the pending litigation news. Covid has certainly slowed down the court systems, but now that things are opening up again, perhaps they can get back on track.

I’m sure one can get a better sense of timing with deeper diligence, but without knowing that, we must either wait until we have more information, or keep any potential trades extremely small (no point in gambling). Perhaps this would make a good addition to one’s Speculation Sandbox?

For a trade, my preference would be to buy the longest dated options expiring in 18 months (so that we can buy as much time as possible), and then as time passes, re-evaluate whether to buy new options expiring even further in the future (as available), as new information is revealed.

Options expiring in 18 months are currently priced as follows (see left 2 columns):

The $7 strike options have a very significant bid-ask spread so we will ignore those.

Below is the return profile, at expiration, for the remaining options:

As expected, the table above indicates some pretty great asymmetric outcomes!

One potential trade could be to buy a combination of the $12, $15 and $17 strike calls, and reserve cash for future purchases.

In the worst case, the options could expire worthless. So we must manage that risk with appropriate position sizing.

Closing Thoughts

Mai recognized that markets tend to over-discount uncertainty from identified risks.

Events that create the perception of going concern risk can therefore create options mis-pricings, and as a result we can have the opportunity to create bets where the expected probability-weighted gain is asymmetric compared to the probability-weighted loss: Heads, You Win Big, Tails You Lose Little.

If the identified risks end up being not as bad as the market anticipated, the asymmetric bets identified above can result in massive wealth building outcomes.

As an outsider of the Pharma industry, TEVA sure seems like it could turn out to be one such highly asymmetric outcome.

Would You Take This Bet?

Why/Why not?

Do you know much about Pharma Litigation?

If you, or anyone you know, could help me shed more light on the legal liabilities TEVA faces, I’d love to speak with you. Do please get in touch. Thanks!

If you enjoyed this article, share it with a friend, they may like it too!

Help spread the word about Playing For Doubles.

Thank you and Happy Investing!

Disclaimer:

Of course, as always, none of the above is investment advice.