The Cost of Hedging With PUTs

Thoughts On Hedging (Part 2)

This is my second article on Hedging.

During Part 1, we discussed the following:

What is Hedging?

Why Hedge?

And How We Can Hedge?

Recall that hedging is the cost of insurance against a potential stock market drop. By definition, hedging is a waste of money... most of the time.

Just think about how many months of car insurance premiums you’ve paid vs used. Sometimes however, insurance comes in handy.

With that in mind, today, I want to go into more details about how we can hedge using PUT options. If you’re new to options, you can learn more here:

In order to hedge with PUTs, you need to answer the following questions:

What You Will Hedge With?

How Long You Want To Hedge For?

How Much Are You Willing To Spend On Your Hedge & When Will Your Hedges Kick In?

Hedging With ETF PUTs

To hedge with PUTs, you can buy Puts on each individual stock you own. However, if you have several in your portfolio, that could become costly and cumbersome.

Alternatively you could buy PUTs on an ETF that closely resembles the makeup of your portfolio. For example, if you own a lot of high growth companies (Mavericks tend to fall into this category), you could consider buying PUTs for the QQQ or IWO. If you own a lot of large well-known American businesses, perhaps SPY may be a better alternative.

For the purpose of our discussion, we will use SPY.

How Long To Hedge For?

This is a personal decision. The longer the time period, the more expensive the hedge will be. But of course, the longer your portfolio will be insured.

Markets always go down faster than they go up, so very long hedges aren’t always needed. Of course you’ll never know the perfect time frame beforehand.

Ask yourself why you are hedging. The reason will help you choose your hedging timeframe. For example, today we live in a very uncertain world. There is uncertainty about the impact of opening up the economy, how company earnings will be impacted in Q2, progress towards the COVID vaccine and other treatments, and looking forward, perhaps even November US presidential elections. News about all of these can impact stock prices.

Based on the above key points of uncertainty, perhaps a 3-6 month hedging time frame is ok. During this period, several of the above open questions may get answered or at least we may have more clarity about them, relatively speaking.

How Much To Spend On Your Hedges? And When Will They Take Affect?

This is once again a personal decision.

The strike prices you choose for your PUT hedges will be based on how much you think the market will fall AND how much of a drop you’re willing to stomach.

This is what makes hedging challenging.

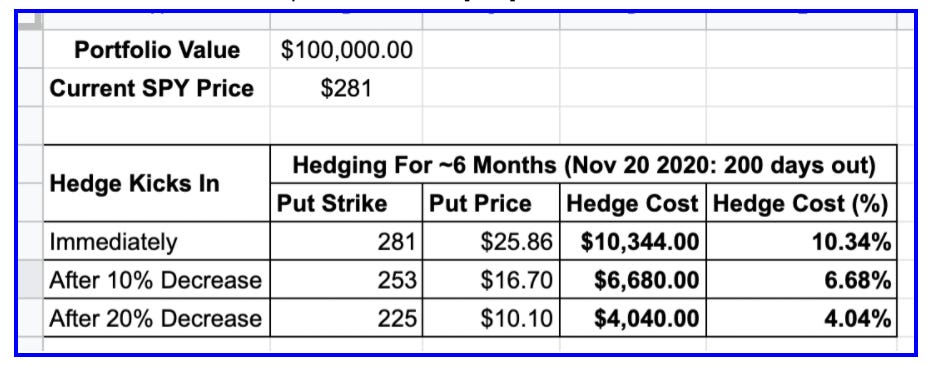

Assuming a portfolio worth $100,000, let’s look at a few different scenarios.

Hedging For 3 Months

If we hedge our portfolio with SPY Puts for about 3 months, the below table shows our PUT strikes and our hedging costs. Note, since there are no options that expire in exactly 3 months, I have chosen the closest expiration, which is August 21, 2020, 109 days away.

Since our portfolio is $100,000, that is equivalent to roughly 355 shares of SPY. Since each option controls 100 shares, to hedge 100% of our portfolio, we would need to purchase 4 PUTs. Yes, we are over-hedging here unfortunately, by 0.45 PUTs, because we cannot purchase partial options.

Note: You can view details in the spreadsheet here.

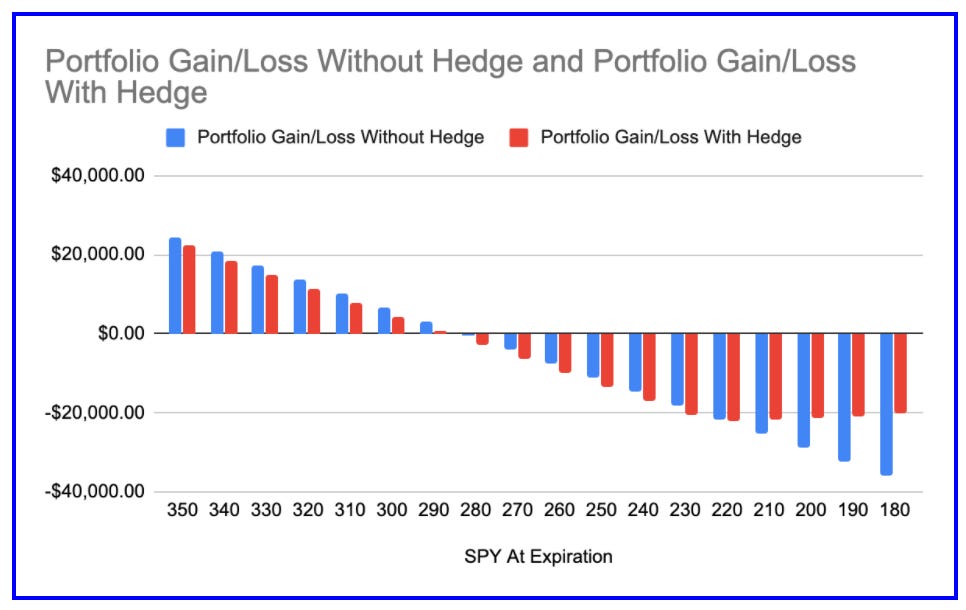

Hedge Immediately (i.e PUT Strike = $281)

Looking at the below charts, we can see that the hedge starts to kick-in if the market were to fall below $281 in 3 months.

Hedge After a 10% Decline (i.e PUT Strike = $253)

Similarly, we can see that the hedge starts to kick-in if the market were to fall below $253 in 3 months.

Hedge After a 20% Decline (i.e PUT Strike = $225)

Once again we can see that the hedge starts to kick-in if the market were to fall below $225 in 3 months.

A Few Takeaways

Hedges Are Expensive Today: Notice that the most expensive hedge is when we choose a strike price closest to the ETF price, namely $281. For just a 3 month hedge, it costs us $7,980 (4 contracts x 100 x $19.95 per contract) or almost 8% of our portfolio. A couple of months ago, this same hedge would probably have cost less than ~3%!

Out Of the Money Hedges Have Lower Out Of Pocket Expenses: If we wanted our hedge to kick-in after the market drops 10% or 20%, it would cost us a lot less up front, $4532 and $2348 respectively.

Keep in Mind Total Portfolio Loss Potential: Even though out of the money hedges cost us less up front, the actual portfolio would need to be down 10% and 20% before the hedges kick-in. As a result, the total loss on the portfolio is considerably higher (14.5% and 22.28% respectively). That’s the trade-off.

A person who justifies buying these lower strike PUTs is saying “I am willing to endure my portfolio dropping 10-20% before relying on any hedges.”

And this may be ok...they’re willing to accept 10-20% portfolio volatility. As I said above, this is a personal decision based on your own risk tolerance.

Current Hedges Won’t Keep Up With Portfolio Losses: Notice that even in the scenarios where the market falls a significant amount, the gains from the hedges fail to keep up with the portfolio losses. That is, hedging is not free. The benefit of hedging is that it stops our portfolio from falling as much it would have otherwise. But this benefit costs money, as it should.

A Six Month Hedge is More Expensive Up Front: As one would expect, hedging for 6 months is more expensive than hedging for 3 months, as shown below. Detailed charts can be found in the Spreadsheet here: [Link]

A Six Month Hedge May Be Cheaper If You Plan To Hedge For An Extended Period Of Time: If you believe we are going to be in a difficult market environment for a long amount of time, a more expensive 6 month hedge may be better. That is, two 3-month hedges would cost a lot more than one 6-month hedge.

As you can see, there are many nuances to hedging. Hopefully the above gives you a good sense of the different factors one needs to consider when putting on a hedge. It’s always better to hedge before there is fear in the market. This is what makes hedging difficult!

Questions For You:

Based on the above cost of hedging, would you hedge today? Why or Why Not?

Can you think of how we can reduce our cost of hedging? What would the tradeoffs be?