Using Claude.AI to Estimate Brand Value

Using Claude.AI to Estimate Brand Value

How AI Helped My Investment Process

If you like this article, please ❤️ it above and forward it to a friend :)

If you’re new here, I am a fan of the Coffee Can Portfolio, an “Active Passive” approach to investing. The idea of a Coffee Can is simple: Buy a basket of the best stocks you can and let them sit for years. You incur no costs with such a portfolio, and it is simple to manage.

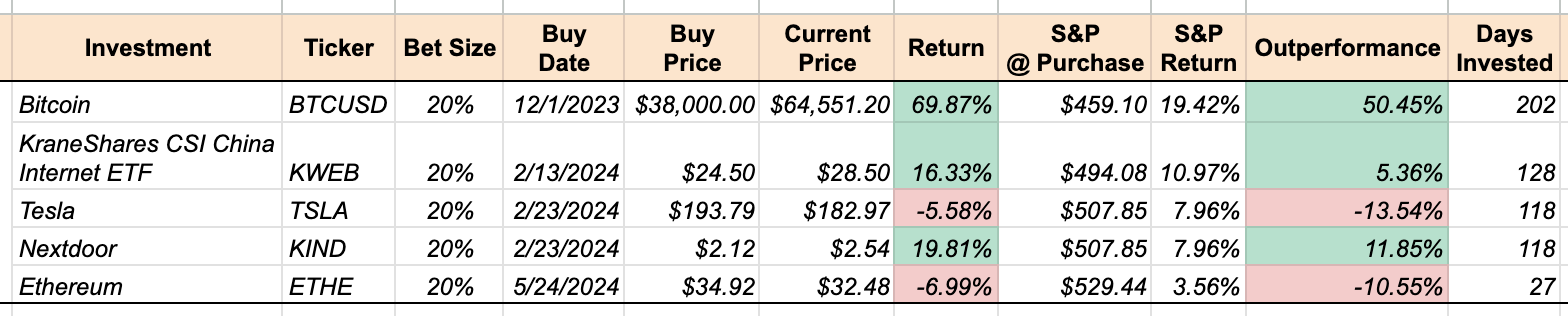

Latest Coffee Can Results To Date:

Thoughts on the above investments:

I’m curious about how to leverage AI to enhance my investment process. I’m sure this will soon become common practice, if it hasn’t already. So this article is about how I used Claude.ai to help me evaluate an investment opportunity I alluded to earlier.

Last month, I wrote that the stock market can sometimes create investments opportunities where we can buy a company for less than its brand value. GoPro might be one such company.

Lets see whether its brand value exceeds its market value.

But, before I begin, a question:

Have you used AI in your investment process?

I’d love to learn more about the tools you’ve used, and what you have found to be most helpful. Please do reply to this email, thank you!

The Power of a Strong Brand

We live in a world where, unlike before, the vast majority of a company’s value can come from intangible assets. Brands are a huge component of this.

Why? Because a strong brand wields significant power in the marketplace and can greatly influence consumer behavior.

The power of a strong brand lies in several key aspects, for example:

Customer Loyalty: Strong brands create loyal customers who are more likely to choose the brand repeatedly, even in the face of competition.

Premium Prices: Consumers are often willing to pay more for a strong brand, as they perceive added value and quality.

Switching Costs: Established brands can make it difficult for new competitors to enter the market, as consumers may be hesitant to switch to an unknown brand.

Extension Opportunities: Strong brands can leverage their reputation to expand into new product categories or markets.

Negotiating Power: Strong brands have more negotiating power with suppliers, distributors, and other partners. They can secure better shelf space, more favorable contract terms, increased marketing support etc.

Attracting Talent: Companies with strong and growing brands can be seen as desirable places to work.

Lastly, while no brand is immune to crises, strong brands are more resilient and can recover more quickly from negative events. Consumers are more likely to forgive and continue supporting a brand they trust and value.

All of the above attributes directly lead to higher turnover and/or profit margins, and as a result higher market value.

Claude.AI, How Would You Estimate Brand Value?

When I wrote that GoPro might be a company whose brand value exceeds its market value, this claim was based simply on intuition.

So I asked Claude.ai to see whether it could help me quantify this claim. Perhaps that would get closer to the conviction required for a potential investment.

I’m not a branding expert, so I asked Claude to tell me how.

Here are a few approaches he (it?) listed:

The Royalty Savings Method:

Assumes that if a company did not own the brand, it would need to license it from a third party and pay royalties for its use. The value of the brand is therefore estimated by calculating the present value of the hypothetical royalty payments that the company is relieved from paying because it owns the brand.

Price Premium Method:

Calculates the value of a brand based on the price premium that the branded products command compared to generic or unbranded alternatives.

The Cost Approach:

Calculates the value of a brand based on the accumulated costs incurred to create, develop, and maintain the brand over time.

Replacement Cost Method:

Estimates the value of a brand by determining the cost to recreate or replace the brand from scratch, considering current market conditions.

Econometric Modeling:

Uses statistical techniques to isolate the impact of a brand on a company's financial performance, considering various factors like market share, price elasticity, advertising effectiveness etc.

Let's calculate brand value based on a few of these.

The Royalty Savings Method

Step 1: Determine GoPro's brand-specific revenue

GoPro's trailing 12 month revenue was ~$986 million.

What % of the revenue is accounted for by the brand?

30% of sales come from gopro.com

70% of sales come from retail channels

If we assume 50% of retail sales, and 100% of gopro.com sales are driven by the brand, then GoPro’s brand revenue = $986 million × 65% = $641 million.

Step 2: Assess GoPro's brand strength and royalty rate

Based on GoPro's strong brand recognition in the action camera market, assume a royalty rate of 4% (per Claude, this rate is an assumption based on industry benchmarks for well-established niche brands).

Step 3: Project Royalty Income

Case 1: No Brand Growth

0% Growth rate per year for 5 years

therefore:

Year 1 royalty: $39.44 million

Year 2 royalty: $39.44 million

Year 3 royalty: $39.44 million

Year 4 royalty: $39.44 million

Year 5 royalty: $39.44 million

Case 2: Brand Decline

-5% Growth rate per year for 5 years

therefore:

Year 1 royalty: $37.47 million

Year 2 royalty: $35.59 million

Year 3 royalty: $33.81 million

Year 4 royalty: $32.12 million

Year 5 royalty: $30.52 million

Case 3: Modest Brand Growth

2% Growth rate per year for 5 years

therefore:

Year 1 royalty: $40.23 million

Year 2 royalty: $41.03 million

Year 3 royalty: $41.85 million

Year 4 royalty: $42.69 million

Year 5 royalty: $43.54 million

Calculate the present value of the projected royalty income

My former boss used to say, a DCF is largely an exercise in creative writing…

so let's get creative!

To come up with a terminal value, we can be super conservative by estimating a 20% discount rate. Lets also use zero growth after year 5.

This gives us a Present Value of

Case 1 (No Brand Growth): $351 million

Case 2 (Brand Decline): $286 million

Case 3 (Modest Brand Growth): $381 million

All of these are greater than GoPro’s current enterprise value of ~$195 million.

The Cost and Replacement Cost Approaches

It’s difficult to say how much of a company’s historical marketing/advertising expenses should be attributed to creating, developing and maintaining its brand. That said, just looking at the past few years of income statements, we see 100s of millions of dollars worth of marketing spend.

So I think we can safely assume the cost approach would give us a number significantly higher than GoPro’s current enterprise value.

It’s also a pretty safe assumption that replacement cost > actual cost so once again we can ascertain that this number is higher than GoPro’s current enterprise value.

Does That Mean This Is An Opportunity?

Well, not necessarily. The above analysis has some holes.

For example, perhaps a 4% royalty rate on a physical product like a camera makes sense. However, GoPro has a healthy subscription business, which should warrant much higher royalties. We need to adjust for that.

More importantly, if brand value is the primary basis for our investment thesis, we must ask ourselves whether the brand has staying power? Will it remain relevant going forward or will it degrade?

Unfortunately, company revenues have declined since 2021 and these revenue declines are accelerating (down ~6% and ~8% in 2022 and 2023 respectively). So Case 2 (Brand Decline) above, which assumes a 5% decline for the next 5 years may not be conservative enough…

Unfortunately, the CEO’s outlook and notes on recent trends don't give me much confidence.

This tells me the brand doesn’t have great pricing power.

It also implies a lack of consumer loyalty.

Consumer behavior isn’t reflecting the reasons that make a strong brand (listed above).

That’s not what we want to see.

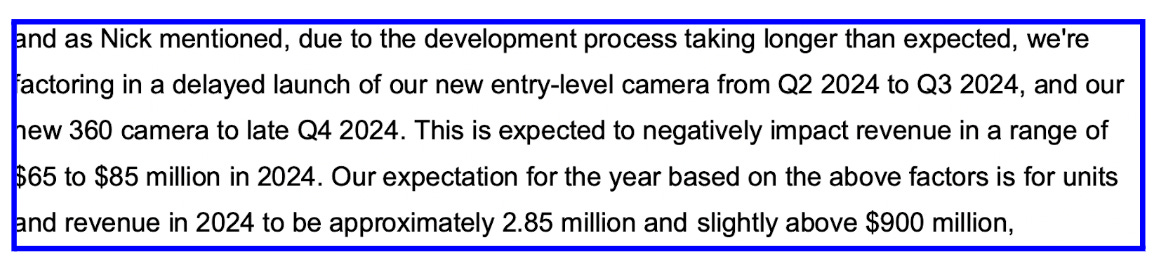

Next, GoPro doesn’t seem like a company in control. It is continuing to shoot itself in the foot. They are expecting delays in their new entry-level camera and as a result forecast further revenue declines (up to 8%) in 2024.

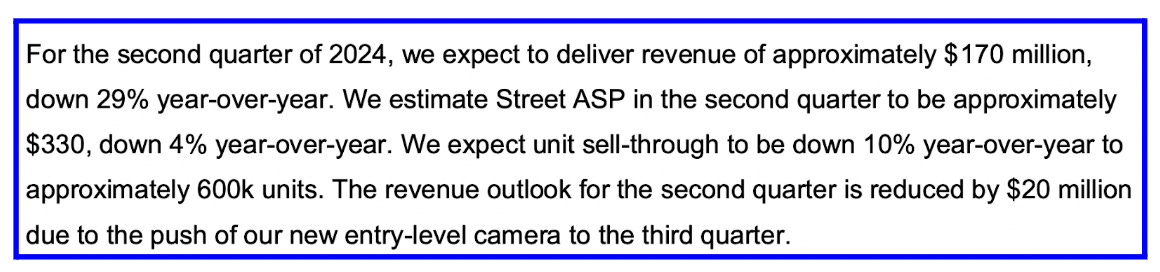

More bad news:

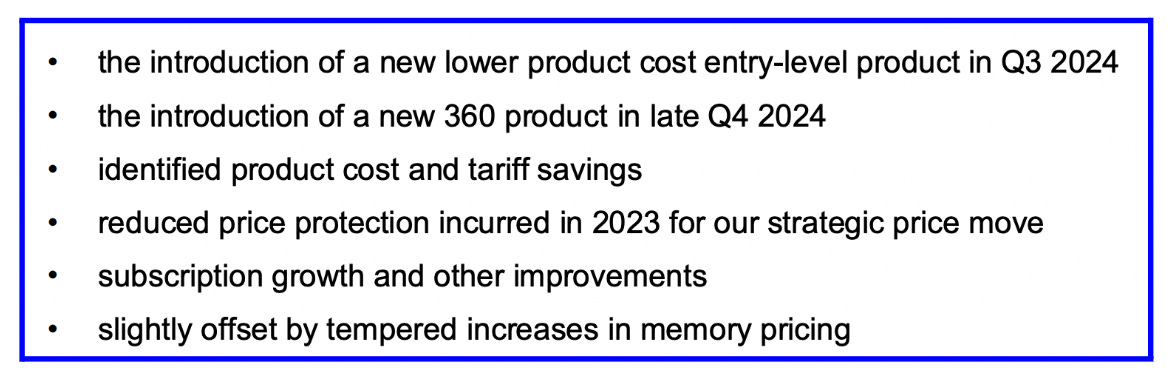

That said, the company somehow believes they will improve margins in the second half of the year, due to the following reasons. Do you believe them?

It’s a tough sell, frankly.

Question:

If you are a GoPro fan or customer, how do you feel about their brand strength? Comment below or reply to this email.

Where To From Here?

On the one hand, I do believe the brand is worth more than the business today. But it feels like the brand is also losing value. That’s concerning.

To a strategic buyer, the brand may be worth more than GoPro’s current enterprise value. But I’m not one to invest in a company simply hoping for it to get acquired. Plus, why hasn’t that happened yet?

So where to from here?

We have two options:

Put this opportunity in the “Too Hard” pile, and move on… OR

Dig deeper. Here are a few ideas:

Find GoPro customers to get a better perspective about how they view the brand, and better understand why they haven’t been buying from GoPro as much as they used to.

Go talk to BestBuy employees to see how potential customers feel about GoPro, and how hard it is to sell to them.

Find GoPro employees to hear what they think.

This company isn’t a Maverick, perhaps it once was. So I’m inclined to move on and find a different company to investigate.

Did AI Help with the above analysis?

Yes and no.

Yes, because it greatly reduced the time it would have taken to perform the above analysis. It helped me to quickly figure out different approaches I could use to quantify my perception of brand value. It also provided step-by-step instructions on how to perform the calculations.

As a generalist investor, I found this to be super helpful. (Using Google would have taken significantly longer).

But you have to be careful simply relying on the numbers AI uses. It seems to just make them up!

That said, Claude wasn’t a substitute for my analysis. It wasn’t able to synthesize an investment case for me. I had to do that.

It really showed me the importance of getting better at “prompt engineering”, that is, getting better at asking better questions, in order to get better answers from the AI.

Where Can AI Help?

The investment process is like peeling back the layers of an onion to reveal the core truth about a company’s potential. It involves multiple steps:

Company Sourcing

Industry Analysis

Company Analysis

Financial Forecasting

Valuation

Investment Synthesis

Steps 1-3 seem like areas where AI could speed up the process of acquiring the information needed. For example, for Company Sourcing, I can see a future where AI could significantly improve today’s screening processes. With AI I should be able to search like this:

Find me a list of all Crypto companies worth less than $1 Billion, where a former colleague of mine currently works.

Find me a list of companies whose founder just returned as CEO in the past 6 month.

Find me a list of companies operating in an oligopoly industry structure, but growing at least 2X faster than the incumbents of that industry.

etc

Steps 4-6 require more hypotheses, inference, insights and iteration. These seem like areas where AI needs more time to get better.

That said, I wonder how hard it would be to train AI based on past successful investments, like the ones we have explored so far (NVR in 2001, COST in 2005, AMZN in 2012)?

If you’ve had any experience building AI Agents or programming LLMs, let me know if you’d like to collaborate.

Happy Investing!