NVR's Secret to Reducing Risk and Boosting Returns

NVR's Secret to Reducing Risk and Boosting Returns

And How We Can Apply It To Stocks

If you like this article, please share it with a friend & click the ❤️ above. Thank you :)

Quick tidbit about Tesla: As you must have noticed, Tesla stock has been on fire lately. Yesterday, it was up 10% primarily because they reported that their Energy & Storage deliveries were up over 130% QoQ.

What is the lesson in that? Great companies surprise to the upside!

That’s why we Invest in Mavericks.

Latest Coffee Can:

NVR's Secret to Reducing Risk and Boosting Returns

NVR, a homebuilder, has been one of the best performing stocks of the past several decades. One ingenious thing they did is to use options to control pieces of land rather than buying the land outright. This helped them limit their downside risk, while simultaneously participate in the upside of the land development.

This is a very powerful idea.

Similarly, we can control large amounts of stock (for years at a time) with relatively small amounts of capital. By doing so, like NVR, we can reduce our downside, but also participate in the stock’s upside.

We can do this using options.

If you’re unfamiliar with options, read my Fun With Options Series:

Let’s walk through a real-world example.

Applying NVR’s Operating Model to Alibaba Stock

Let's explore how we can apply NVR’s operating model to stocks using a hypothetical investment in the Alibaba Group.

One could argue that The Alibaba Group is quite undervalued. If we look forward to 2030, a projected EBITDA of $30 billion with a 10x multiple gives us a $300 billion market cap. Add to that net invested assets of $200 billion, and we get $500 billion. The stock is currently trading just under $180 billion. One could even argue that this is quite conservative. By comparison, Amazon has an EBITDA multiple of over 20, while Alibaba’s current multiple is 6ish. If the investment thesis plays out, that gives us at least a ~3X upside in ~5.5 years (about ~22% per annum). Not bad at all.

The above “undervaluation” however is nothing new. Many investors started saying that BABA was undervalued when the price was significantly higher than it is today. Unfortunately, if they bought the stock, they are likely significantly underwater on their investment.

How can we avoid such a drawdown if we decide to invest in Alibaba today?

By buying long term BABA 0.00%↑ call options instead of the stock, we can control all the Alibaba stock we would have purchased, limit our downside investment risk, and maintain the large majority of the upside potential.

To demonstrate, let’s discuss:

Which Options Should We Buy?

What’s The Return Profile Of Owning The Stock vs The Options?

What Can We Do Once The Options Expire?

1. Which BABA Options Should We Buy?

Long term options allow us to invest only a small amount (relative to our capital base) in order to buy enough time for the investment to prove itself.

NVR did this by pre-selling homes and collecting deposits. If successful, then it would exercise it’s land options to purchase the land.

As stock owners, our job is simpler, we simply have to wait and see whether the stock price appreciates before expiration.

Since we’re buying time, I would buy options with the furthest expiration date. In Alibaba’s case, that is 18 Dec 2026.

As for the strike price selection:

The higher the strike price, the cheaper the option, the lower our initial capital outlay, therefore the lower our risk of losing the option premium.

The lower the strike price, the lower the stock price needs to be in order for our option to be worth something at expiration. So it costs more.

I would choose an option contract as close to 70 delta where I do not deploy more than 20-25% of the capital I would have used had I simply bought the stock. Why? If the stock goes against us, this is the max we lose, and a 25% loss would fit into the Optimal ROI I am aiming for.

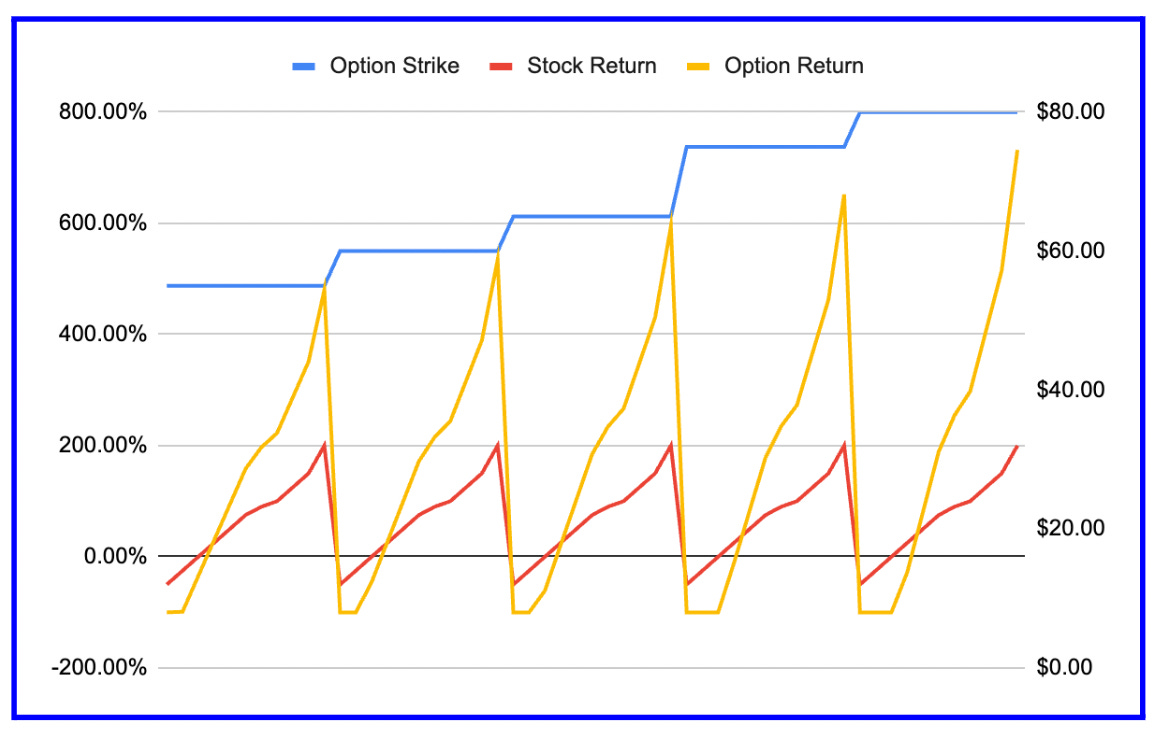

2. BABA Return Profile (Stock vs Options)

Here the are the profits and losses of several potential options contracts we could purchase.

Vertical Axis: The left axis is the % return. The right axis is the strike price.

Horizontal Axis: Modeling results where the stock return ranges from -50% to +200%.

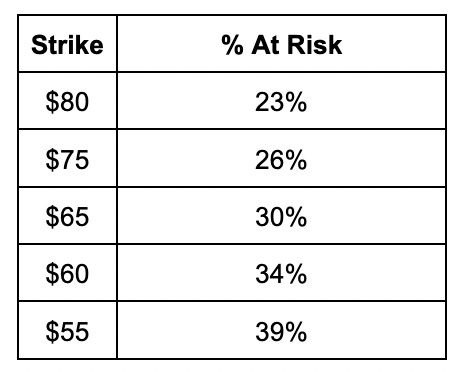

I’d likely choose the $80 strike options, because the others require a much higher amount of capital at risk. This is one way we are protecting our downside. Of course, you could reduce the % at risk even further by going more out of the money. But the higher you go, the higher the leverage. To each their own…

Note: If our position size is say $100,000, we would buy $23,000 worth of the December 18 2026 $80 Calls.

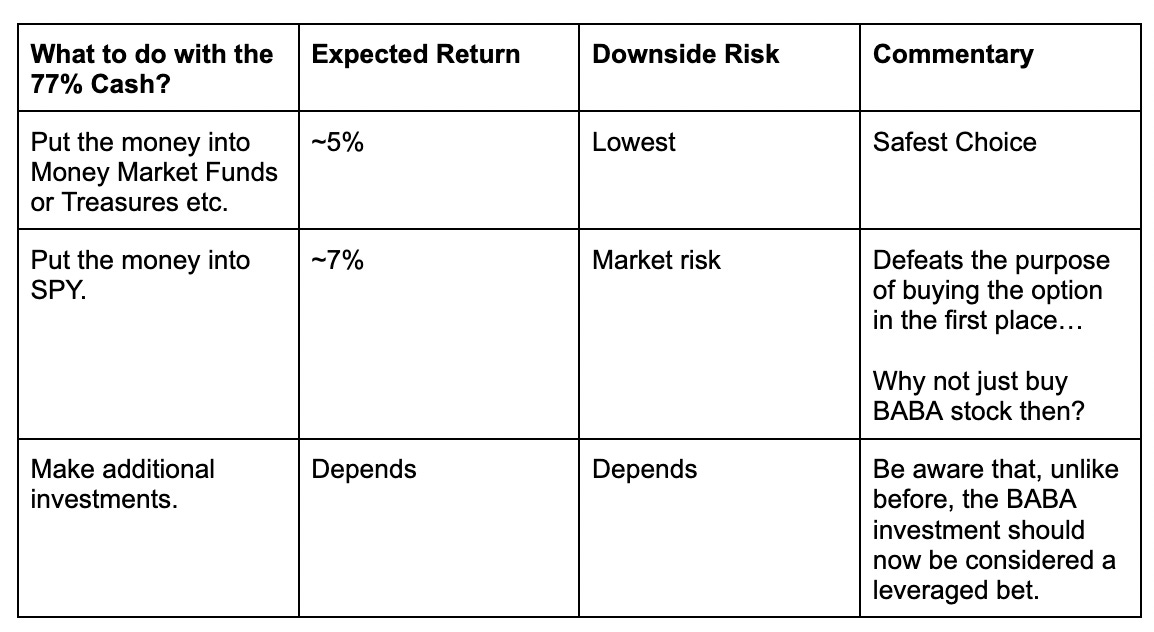

Since we are only risking 23% of our position size, what do we do with the remaining 77% of our cash?

We’re going to go with the safest choice, put the money into the Money Market.

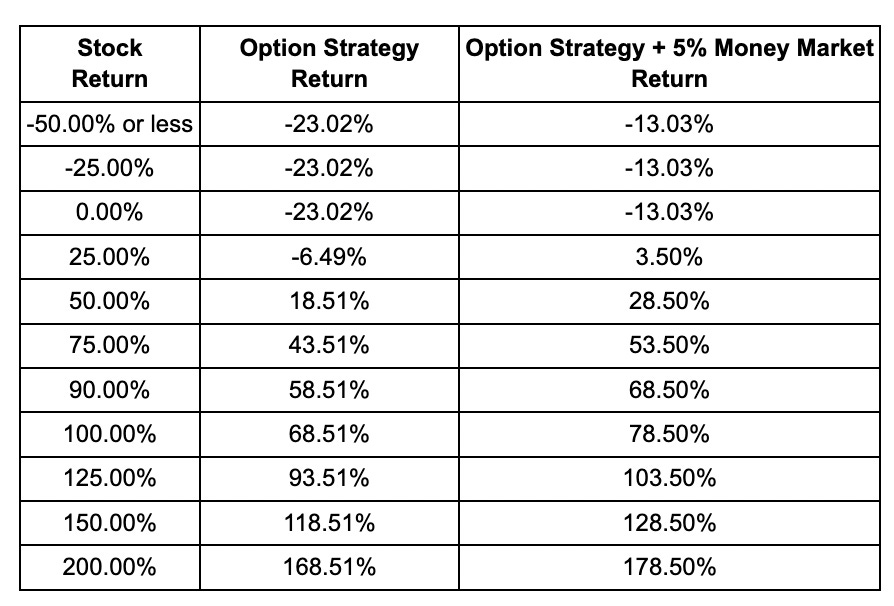

Based on this, we get the following return profile.

Notice what happens to our max downside: it reduces to only -13!

How?

Because the options expire in 2.5 years. During this time, our Money Market return is roughly ~10% (77% * (1.05^2.5 - 1)).

What Does This Accomplish?

Let me show you.

Assuming equal sized bets, we know that an investment strategy has a positive expected value when

Win to Loss Ratio > (1 - Batting Average) / Batting Average

Let’s calculate these empirical values from our Investment Scorecard. In the scorecard, I have shared 72 bets so far (yes, a few of the bets are still active, and yes they were not all equal sized bets, but work with me here…).

Our batting average is ~64% (46/72).

Our Win to Loss Ratio is 3.4 to 1 (178/53)

So the expected value is quite positive.

But what’s our new W:L Ratio?

If we always use the options strategy above:

The new denominator is 13%.

Assumes all our losing bets go to zero.

Assumes we get 5% risk-free rate returns.

Assume all bets are 2.5 years long.

The new numerator is around 75% of the original.

On avg, our upside (compared to if we simply bought the stock) decreases by ~25%.

This means our new W/L ratio is ~10.3 to 1.

That’s 3X the original!

All we did was change the financial instrument we purchased, and we:

Significantly reduced our downside (by 75%! (53% → 13%))

Maintained the majority of our upside (about 75%)

Increased our win to loss ratio (3x)

What does this accomplish?

As a consequence, we have now afforded ourselves the ability to have a lower batting average, and still maintain a positive expectation investment strategy.

How cool is that? !

Some Things To Be Aware Of

The above strategy will not work if:

The stock has no options.

The options don’t expire far into the future.

The options are illiquid and have significant bid-ask spreads.

If your average loss is not as high as above, your W:L ratio might not benefit as much.

Perhaps this approach works better when investing in large companies only, as they are more likely to have long dated options.

Note: We could also use some more involved options strategies to reduce our risk further, and also to increase our winners’ upside, but I haven’t really gone into all that in this article. If you’d like to discuss that, feel free to email me.

3. What To Do Once The Options Expire?

Ok, if we decide to pursue the above strategy, what do we do at expiration? Here are some choices:

Scenario 1: Stock Is Significantly Above Strike Price

This is the ideal outcome.

At expiration, depending on our assessment of the stock’s fair value, we can choose to:

Sell the options and realize long term capital gains.

Exercise our right to buy the stock at the option strike price, and become shareholders in BABA with significant unrealized long term capital gains.

Roll our options into a future expiration (if you’re not sure what this is, don’t worry about it or feel free to email me and I will explain it to you)

Scenario 2: Stock Is Slightly Above Strike Price

In this scenario, we likely had a small loss or a small gain.

If the stock price - strike price > premium paid, then our option would be profitable. Otherwise, it would be unprofitable.

We could sell our options and move on or if we still believe in Alibaba, we could consider repeating our strategy and buy more options that expire a few years in the future (or of course, we could just buy the stock).

Scenario 3: Stock Is Below Strike Price

In this case, our options expire worthless.

That is, we lose the full amount we had put at risk. That said, we have only lost ~13% of our intended position size. That’s not bad at all. It’s the extremely large losses that we want to avoid.

Had we used this strategy in 2022, when BABA was already considered undervalued by many, we’d be far better off than BABA stockholders, who are likely down ~50%.

So what do we do in this case? We could accept our loss and move on since the investment didn’t work. Or if we still believe in Alibaba, we could consider repeating our strategy and buy more options that expire a few years in the future (or of course, just buy the stock).