An Analysis of 100 Baggers

An Analysis of 100 Baggers

And, are Mavericks good candidates to 100X?

It’s my birthday! So if you like this article, please do share it with a friend or click the ❤️ above. Thank you :)

If you’re new here, I am a fan of the Coffee Can Portfolio, an “Active Passive” approach to investing. The idea of a Coffee Can is simple: Buy a basket of the best stocks you can and let them sit for years. You incur no costs with such a portfolio, and it is simple to manage.

Here are the current results of my latest coffee can:

Thoughts on Bitcoin, KWEB, Tesla, and Nextdoor

I came across an interesting PDF online titled “An Analysis of 100-Baggers”, where the author (Tony) shared several examples of 100-baggers.

Here are my biggest takeaways after reading it. I believe these can be helpful in identifying future multi-baggers (not just 100-baggers).

1. Look For Earnings Growth PLUS Multiple Expansion

Tony pointed out that the most powerful stock moves happened during extended periods of time of growing earnings AND expansion of the PE ratio.

We can see how powerful such a combination can be. For example, take a stock with a EPS of $0.5/share and a PE ratio of 10. If we can see a path of EPS growth to $2.5/share, with no change in the PE multiple, that should result in a 5 bagger. However, if the market were to reward this EPS growth with a PE of 30, that would in-turn turn into a whopping 15 bagger! That's a powerful dynamic to keep in mind when evaluating stock appreciation potential.

We must be careful however because the reverse is also true. If earnings growth slows, the market will likely punish the stock by reducing the PE ratio. As a result, this could significantly dampen results.

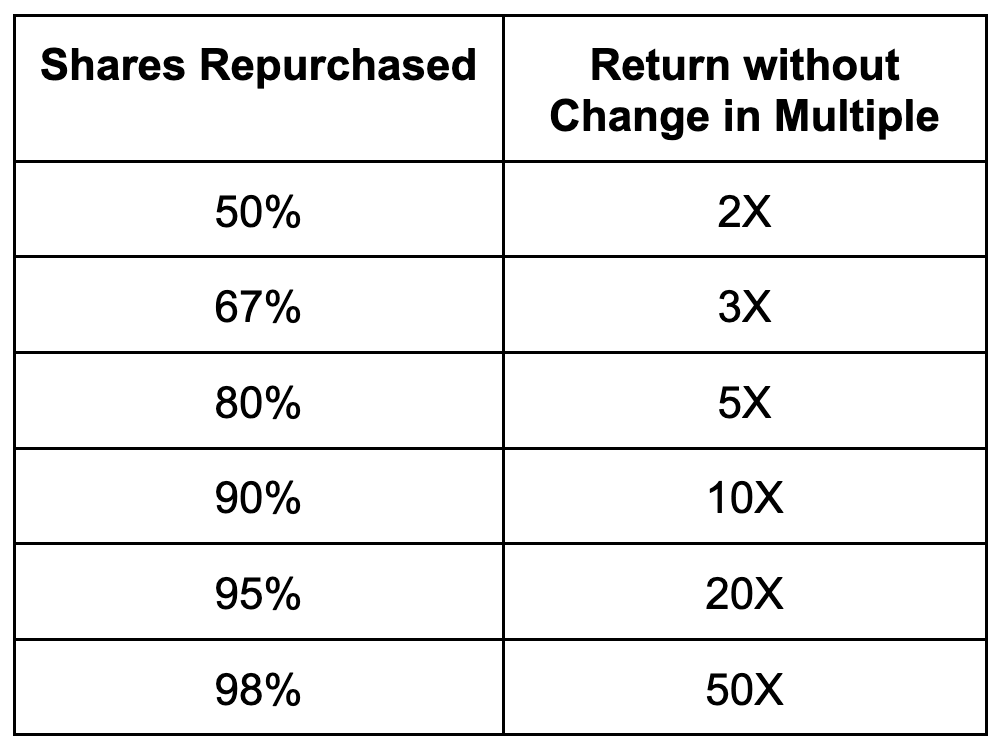

Note: Yes, stock buy-backs can also be a source of stock price appreciation. That said, they only meaningfully add to returns after a significant percentage of company shares have been purchased (and this usually takes a long time).

2. Accelerated Earnings Growth is Rewarded with Multiple Expansion

Tony also pointed out that periods of PE expansion often coincide with periods of accelerating earnings growth.

Sequential, quarter over quarter growth in particular is highly coveted by the market.

This creates an interesting dynamic. Accelerating earnings growth rates can be less sustainable than steady growth rates over long periods of time. But tend to be well rewarded by the market in the near term.

3. When Earnings Growth Slows, Watch Out

If a stock experiences significant earnings growth in a relatively short amount of time, you have to be very careful.

For example, in 2020, covid-dynamics led to much faster growth rates for several companies resulting in a pull-forward of future earnings. Post covid, when earnings growth slowed, many of these companies had pretty significant stock price declines.

So, if we see a stock with significant potential, where the stock has already made a large move higher, we must really assess how sustainable the accelerated earnings are before deciding whether to buy the stock. We must also feel comfortable with how potentially slower future earnings growth would combat PE contraction.

A recent example: software names like Salesforce ( CRM 0.00%↑ ), ServiceNow ( NOW 0.00%↑ ), and MongoDB ( MDB 0.00%↑ ), all recently had large drops in stock price due to earnings multiple contraction.

4. Pay Attention To Stocks Wall Street Has Been Yawning At

Tony points out that some of the most attractive 100X opportunities have occurred in beaten down, forgotten stocks. Why? Because such stocks lack demand, and as a result, likely have low multiples.

If you can foresee a sustainable improvement in future company fundamentals, then that could be the beginning of a period of significant EPS growth, and a great time to buy the company’s stock.

Note however that it can take multiple years before such stocks get recognized by the market.

5. Tiny Tiny Stocks

One thing that stood out was how small several of these stocks were, at the beginning of their 100X runs. Here are a few examples. Have you heard of any of them?

So, are Mavericks Good Candidates to 100X?

Stage 1 Mavericks (Disruptors), unfortunately, have been staying private longer than they used to, so, as public market investors, having an opportunity to invest in them early has gotten difficult.

When companies came public earlier in their lives, investors used to get many years to observe their operating performance, learn about their markets, and develop conviction before investing in them. When important companies stay private, such information can be harder to obtain or to appreciate.

Unfortunately, I think this is a net negative (and extremely frustrating) for individual investors because a large portion of upside potential is now captured by the Private markets.

But all is not lost. There have been some wonderful public market winners despite this trend. For example, TSLA 0.00%↑ - clearly a Maverick - was worth ~$2 billion market cap at the end of its first day as a publicly traded company, and has been a 100 bagger since. Of course, an outcome like this is very rare however.

It’s important therefore to have the right expectations. 100X is likely unfeasible for Mavericks (as is the case with most stocks). But that’s ok. Here I discuss how big our Homerun investments actually need to be.

On the bright side, Mavericks present a less risky investment option compared to private market investments (usually).

Remember, when we invest in Mavericks, we are looking for companies poised to become the greatest companies of our time. Think Amazon or Netflix in the early 2000s.

When such companies succeed, even as public companies, a 10X outcome (say over 10 years) is a completely reasonable expectation from a Maverick.

In fact, I think it’s likely easier to capture two 10 baggers instead of one 100 bagger in the public markets. (I should do some analysis to validate this hypothesis, but something tells me this is likely to be true).