Eventbrite (Ticker: EB)

A $300M+ Revenue Business For Free

If you like this article, please do share it with a friend & click the ❤️ above. Thanks :)

Eventbrite is the leading ticketing platform for the long tail of in-person events.

Eventbrite IPO’d back in 2018. In hindsight the company was not worth anywhere close to what it was priced at. Today, the stock is ~3.34/sh, down over 90% from a high of $40.25/sh in 2018.

Is this a Buying Opportunity?

I believe so.

What I like about the business:

Price

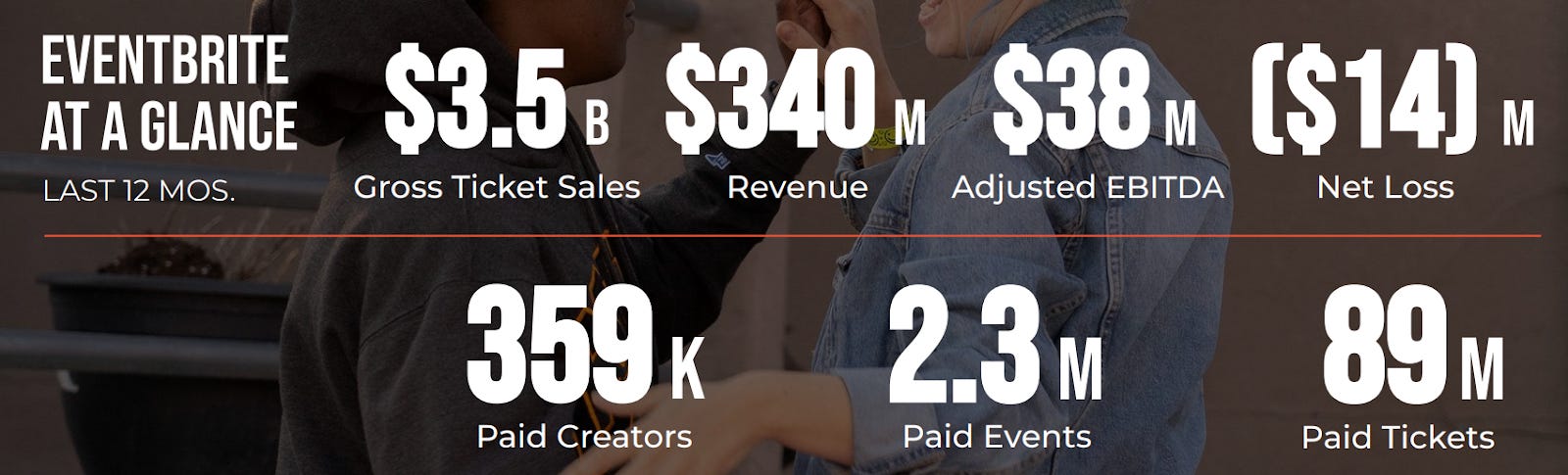

With a market cap of just $320 million, this high gross margin business is currently trading at ~1x revenue, and an enterprise value of just $47 million.

Market Cap: $320 million

Cash + Short Term Investments - Debt = $273 million

Enterprise Value = $47 million

I figure the company’s brand value alone is worth more than $47 million.

So that means we’re getting the operating business, a business with significant scale, for free.

Plus I don’t think one could rebuild Eventbrite today for $47 million. It would likely require much more capital, not to mention several years to get to where it is today.

A few weeks ago, the stock traded down to $2.51/share, which meant Eventbrite had a negative EV! We could have gotten paid to own this company. Although that price didn’t last long, the stock is still very cheap.

Brand & Market Leading Position

Eventbrite is the number 1 player in its market.

It seems to be the default ticketing platform new hosts start with, especially via word of mouth.

Eventbrite has a very recognizable brand. According to the company, if you were to walk down the street and mention Eventbrite, 7 out of 10 people would recognize the brand. That’s quite an accomplishment for any company, let alone a small cap.

The Business Model

High Gross Margins

Negative Working Capital

Low capital requirements to run the business

2-sided marketplace with the potential for strong network effects

Operating Leverage and Future Revenue Optionality

The big opportunity is if it can transition from being viewed as a ticketing platform to a local events discovery platform.

Good news is many folks use Eventbrite for discovery already. That said, it's still early days there…

Eventbrite also has multiple future revenue opportunities it could tap into, once near term challenges have been stabilized:

Growing advertiser tools and revenue

Enhancing event host tools (Pre & Post Events Related Products)

International focus/expansion

During-Event Products (eg: Merchandising)

Other Assets

The company has a significant user base and also owns a unique data set that can be valuable in and of itself.

What Could Be Better?

Network Effects

Although this is a network effects business, their flywheel still seems to have much friction which the company hasn’t been able to remove. To ensure the business gets stronger as it grows, this needs to be remedied.

Event Host Tools

There seems to be an enormous opportunity for better tooling for their event creators. The tools seem clunky. Communicating with event guests can be frustrating. Email marketing functionality is quite basic. Often I hear hosts have to download email contact info into a CSV format so that they can reach out to attendees offline. To name a few…

Walletshare & Pricing Power

Eventbrite’s wallet share has always seemed to lag behind brand mindshare.

Based on my conversations with multiple (smaller) event hosts, folks seem to think Eventbrite pricing is already expensive. We’ve recently seen a decrease in ticketing volume because of this.

As a result, there may not be much latent pricing power left especially for very small events. For example, a recent conversation with a comedian selling 20-30 show tickets at ~$25 per seat doesn’t have a lot of disposable margin to share with EB 0.00%↑ (especially if they are not selling out).

On the flip side, if the platform can (a) become an Event Discovery platform and (b) provide event hosts with better capabilities, Eventbrite’s perceived value and host WTP (willingness to pay) could increase, and simultaneously create better customer lock-in.

Urgency of Outcomes

The company has stagnated (2024 Revenues are not much higher than 2019 revenues).

The management team is finally making changes to help improve the trajectory of the company. We will see whether these work out for them. But I hope management can bring back a more intense sense of urgency back into the company.

In its current form, the company likely faces much friction attracting top tier talent.

So, Is Eventbrite A Maverick?

Yes, I do consider Eventbrite to be a Maverick, a Disruptor. That said, the company hasn’t really been able to graduate past Stage 1.

So why then am I investing?

I view buying Eventbrite as an asymmetric bet offering upside optionality combined with downside resilience:

If the company can stabilize ticket volumes and eventually start growing them again (and become the de facto event discovery platform), this investment can be a homerun.

On the other hand, if the company stagnates and is unable to grow much from here, we are paying next to nothing for the business.

1x revenue

0.14 EV/Revenue

1.35x gross profit

0.2x EV/gross profit

This is a smaller balance sheet based bet, where I plan to wait a few years, and then re-evaluate whether to invest more into this company.

EB 0.00%↑ is the latest entry into Coffee Can 13 with a purchase price of $3.39/share and a purchase date of 8/21/2024.

If you liked this article, please do share it with a friend & click the ❤️ . Thanks :)