BUY KKR: An Undervalued Dependable

One investment approach I am experimenting with is what I call Investing in Dependables, where I look for the following:

Intrinsic Value: Is it virtually guaranteed that the company will be bigger 5+ years from now?

Durability: Does the company have a competitive advantage and is it growing?

Management: Will management be a good, trustworthy representative of my money?

Margin of Safety: Can I buy the business for meaningfully less than it’s worth?

I believe KKR fits this bill. Here’s why.

About The Company:

KKR is a Founder-led Alternative Asset Manager with a 40+ year history. Under the leadership of Henry Kravis, the firm has evolved from a single “buyout fund” to a 1000+ employee asset management firm with offices all over the world.

KKR raises money from institutional investors, and then invests that money on their behalf. It charges both a management and performance fee for this service. Management fees are typically a percentage of the assets being managed, while performance fees are typically a percentage of the profits generated.

The company has a wonderful track record of outperformance over the past 30 years.

So, is the Company Growing Intrinsic Value?

Yes. KKR is growing market share in an industry growing ~12%/year. KKR has grown assets under management at ~18% per year since 2005.

One of their biggest sources of funds is Pension Funds. These funds are seeking ~8% investment returns. Given the low interest rate environment and increasing volatility in the markets, it is unlikely that pension funds and others are going to reduce their allocations to alternative asset managers like KKR any time soon. As a result, KKR’s fee-sources should remain stable.

Separately, there is ample room to continue growing assets under management. KKR’s goal is to be a Top 3 Player in every market they compete in. With KKR’s great brand and track record, they should be able to grow their asset base in markets where their competitors manage significantly more assets today.

The company has also laid out a plan to double both earnings and book value by 2023.

Taking all of the above into consideration, I believe it’s virtually guaranteed that the company will be bigger 5+ years from now.

Durability: Does the company have a competitive advantage and is it growing?

Yes. This is evident by seeing how well the business has scaled.

We can also see that both assets under management and management fees have been scaling faster than their peers.

The cash and investments as a % of total market capitalization is ~60%! This provides good downside protection, but also allows KKR to seed new funding strategies and provide additional capital to close deals. Their size is also an advantage. KKR is one of a handful of firms that can do “mega deals” because of their access to capital on the balance sheet as well as the services of their Capital Markets group.

The strength of their company can be seen from looking at what happened during the Financial Crisis. In 2008, KKR only lost ~$2B in assets under management, a mere 4% of assets. During that time, their management fees actually increased.

Lastly, KKR has associated with it, lots of prestige. It is one of a handful of firms where every Investment Banking associate wants to work after completing their two year banking programs. Finance majors and B-School grads want to work there as well. This gives them access to the best talent pool.

Talent drives strong returns, which increases reputation, which in turn continues to attract assets and talent. And so goes their flywheel.

Management: Will management be good, trustworthy stewards of my money?

Yes. I believe so. Management incentives are aligned with those of shareholders. Employees own more than 40% of the company and have an excellent track record of generating returns and growing assets. 88% of assets under management is Performance Fee eligible, meaning employees will do well when clients do well. As a result, shareholders should do well.

That said, it does feel like the executive / founding team is paid an ungodly amount of annual compensation. This a slight concern.

Margin of Safety: Can I buy the business for less than it’s worth?

Yes, although the price was much better ~6 months ago. That said, I think we can get a satisfactory return at current prices. If you wait for a pullback, it might never come...

KKR is not being given credit for it’s earnings potential because it is currently under-earning.

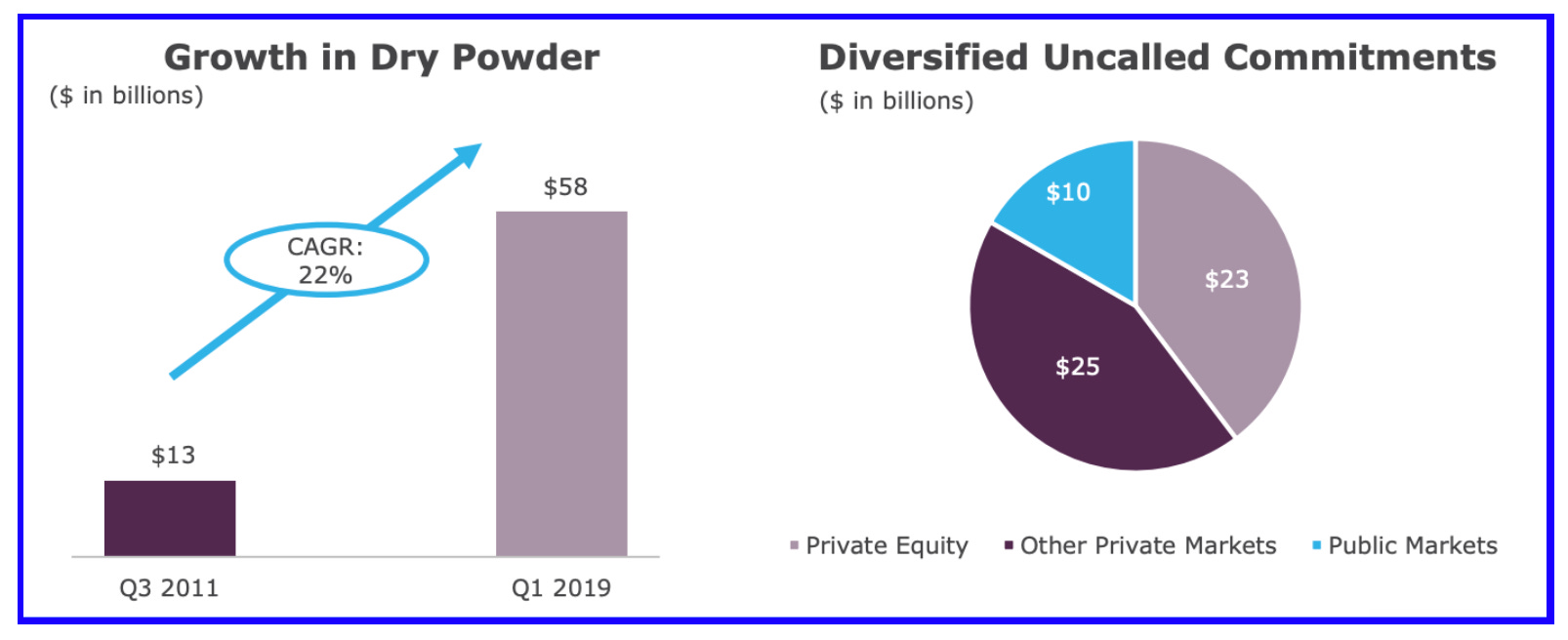

It has roughly $58 Billion in capital committed which hasn’t yet been invested, and hence not earning fees.

Second, a large portion of the currently funded investment strategies are pretty new. These funds, and hence the fees generated by them, will grow over time. Here’s why: Fund profits are small during the initial investment phases. Recall it takes time for an investment thesis to play out. Also, once an initial fund is deployed, a 2nd fund (and future funds) are raised. This means KKR will earn fees from all of these funds concurrently, thereby greatly increasing earnings. This operating leverage should kick in over the next few years.

Valuation:

Net Assets on the Balance Sheet: ~$14/share

Cash: $3+/share

Investments: $13+/share

Unrealized Carried Interest: ~$2/share

Debt: ~4/share

Earnings: ~$2/share

Excluding Balance Sheet assets, we are getting a wonderful business for just a ~6X earnings multiple!

Am I Buying?

Yes. Actually I bought this around $23.40/share.

In conclusion, we have a wonderful stable business whose earnings power is under-appreciated. If KKR can simply meet it’s 5 year plan by 2023, the stock should be in the mid 40s. With a little multiple expansion, I can see a path to doubling or more in the next 5 years (a ~15%/yr return).

That said, one should keep in mind that the $13/share in investments on the balance sheet does include several equities since KKR manages several public market funds. So, if the market declines in the near term, like it did at the end of 2018, KKR’s stock is likely to be volatile. Barring some impairment in the business itself, I would consider that a buying opportunity.

Disclaimer: The above content is for informational purposes only. None of the above should be considered investment advice.

LEARN TO INVEST WITH ME

Subscribe to get weekly investment education and insights sent directly to your inbox.