Advance Auto Parts (Ticker: AAP)

Betting on a Turnaround

If you like this article, please do share it with a friend & click the ❤️ above. Thanks :)

If you’re new here, I share “buy-and-hold portfolios” that I believe can double in 3-5 years.

Here is the performance of our 2 current active portfolios:

You can track my Live Investment Scorecard here.

Next portfolio starting in January 2025.

To receive timely notifications of my buys/sells, join the waitlist here

Advance Auto Parts

If you have been following my Investment Scorecard, you’ll notice I purchased some long term AAP 0.00%↑ Call Options on Nov 22, 2024. For folks who are on the Portfolio Buy-Sell Alerts Waitlist, you should have received an alert about this on the 22nd (if you didn’t, let me know asap!). This investment is up about 40% in ~3 weeks.

Context

Advance Auto Parts is an American automotive aftermarket parts provider (retailer).

The demand for their products is correlated with the following:

Miles driven

Age of vehicles (ideal age: ~7 yrs which is when manufacturer warranties tend to expire)

Number of vehicle registrations (represents future demand)

In the aftermarket auto parts industry, service and availability are what dictates customer loyalty (not price). Having the right parts at the right place at the right time is what drives the auto-parts business. This has been an area where AAP has struggled.

The company’s shortcomings are likely due to several years of management and Board missteps, which has led to years of ineffective execution. Over the past few years, Advance Auto Parts has had:

Execution challenges

Integration issues from past acquisitions

Supply chain inefficiencies

All of which have contributed to much lower margins compared to those of AutoZone and O’Reilly, the leaders in the market.

Despite this, $AAP is the clear #3 player in the market (btw, the top 4 players control only about 40% of market share), and the Advance brand still seems strong.

This creates our opportunity.

The Turnaround Opportunity

$AAP stock peaked at $244 in Dec 2021, fell all the way down to ~$35 in late Oct 2024 ( an 85% decline), and is now trading around $45. The stock may now be bottoming, and Advance Auto Parts may just be a great turnaround bet.

The company has upgraded its Management Team and Board to tackle the turnaround challenges it faces:

CEO Shane O'Kelly joined AAP with a proven track record as former CEO of HD Supply, one of the largest industrial distributors in North America. This is the third time Kelly has had to implement a unified supply chain across companies, something AAP dearly needs.

Tom Seboldt joined the AAP board after spending over 30 years at O'Reilly Automotive. He is well known for his merchandising leadership, another key area where Advance needs help.

Greg Smith joined the AAP board, and is a seasoned supply chain expert with a reputation for large-scale overhauls, which should be helpful as AAP unifies its supply chain operations.

Brent Windom joined the AAP board, and was most recently CEO of Uni-Select, a leading parts distributor.

The good news is all of the above challenges they face are under their own control.

Management has put forward a new plan to help improve operations and margins, and have demonstrated early progress towards their goals.

Advance is closing 700 stores to improve profitability, and will continue to consolidate their supply chain. They also recently sold a business line to significantly improve their cash position by $1.5 Billion (expected to close at the end of year).

These efforts are expected to drive efficiency and cost savings, positioning Advance for long-term success.

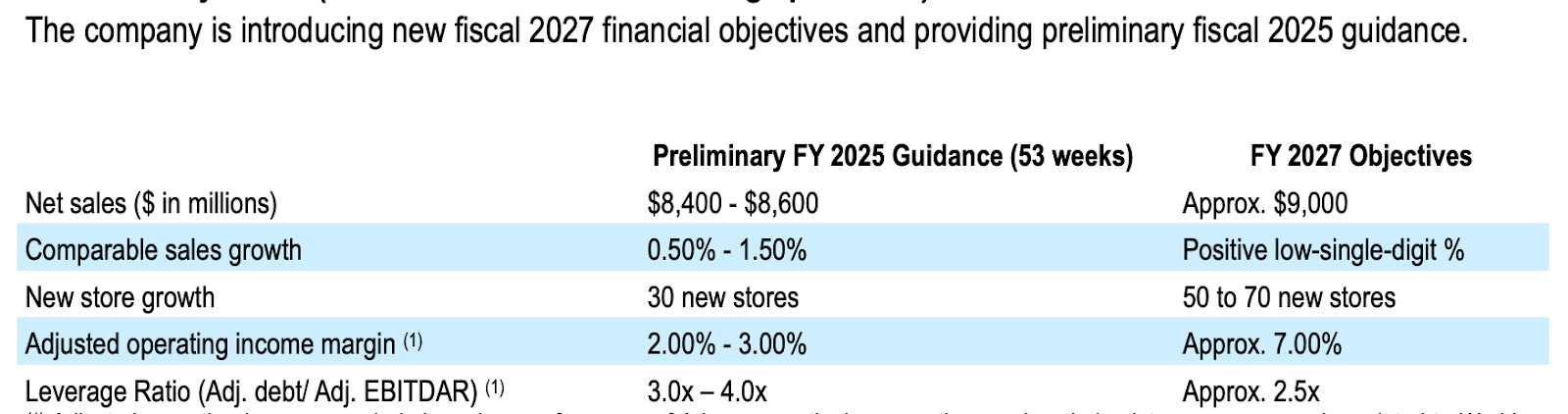

As a result, the company believes it can deliver the following results:

As you can see, the company is projecting $9B in sales with a 7% operating margin by Fiscal 2027. That's about $600 million compared to TTM operating income of just $140 million (more than 4x!). Consensus 2027 EPS is ~3/sh while the above projections should yield EPS of $5-6 per share, which gives us a decent margin of safety if management ends up even remotely close to their projections (which are likely conservative). We can also expect a better multiple at that time if the company has demonstrated progress on its turnaround, is more profitable, is ideally growing same store sales, and has less leverage on the balance sheet.

Advance Auto Parts is admittedly not a Maverick. Nonetheless, I like the risk-reward here.

Is EV Adoption A Threat To The Market?

Short answer: No, not at the moment.

The Bear Case:

Since electric vehicles have fewer moving parts, there is less need for maintenance. Therefore, as electric vehicle adoption increases, the revenues for the aftermarket parts industry will shrink.

In Reality:

It’s unclear how electrification and self driving will impact things in the future. For our investment time horizon however, we only really need to feel confident about the aftermarket parts industry revenue for the next several years.

So let’s do some directional math:

In the US, consumers buy between 13 - 15 million new vehicles per year

In 2023, there were an estimated 292 million registered vehicles in the US

Suppose every one of the 15 million new vehicles sold today is electric, it will take ~5 years just to get to ~20-25% EV market share. By contrast, in 2023, only about 1 million EVs were sold (<7% of total cars sold).

Sure, low-cost EVs which are expected to hit the market next year and beyond, should accelerate this adoption rate. Let's say it doubles to 2 million EVs sold in 2 years, that's 13% market share.

The auto parts market will still have access to 87% of revenues ~9-10 years from now. (assuming $0 aftermarket parts revenue for EVs).

That’s pretty conservative.

It still feels like aftermarket parts revenues will remain quite stable for the majority of the next decade.

Happy Investing!

If you liked this article, please do share it with a friend & click the ❤️. Thanks :)

$AAP looks super interesting. Management team seems to execute strongly. Agree 10X EBIT shouldn't be a stretch if they reach the 7% Operating Margin + Wall Street will project its growth forward which should demand rather 13x EBIT at the time. I am still playing the numbers if an entry at $49 provides enough Upside for the potential Downside. But I love the CEO. I am wondering if he could do to $AAP what Jamie Dimon did to JPM Chase